61

BFRS and BAS Compliance Analysis of Square Pharmaceuticals Limited 1

BFRS and BAS Compliance Analysis of

Square Pharmaceuticals Limited

1

Department of Finance

University of Dhaka

BBA 21st Batch

Course no: F-201

Course Title – Financial Accounting and Reporting

Prepared for:Mohammad Salahuddin Chowdhury

Assistant ProfessorDepartment of FinanceUniversity of Dhaka

Prepared by:Group No. 13

Section: ABBA 21st BatchDepartment of FinanceUniversity of Dhaka

Name Roll no. RemarksTasfia Tasneem Ahmed 21-028

Saif Mahmud 21-067Shahrin Shahid 21-070

Maisha Mushsharat 21-079Protima Saha 21-133

Date of Submission: 20 th June, 2016

2

Letter of Transmittal

June 20, 2016,

Mohammad Salahuddin ChowdhuryAssistant ProfessorDepartment of FinanceUniversity of Dhaka.

Subject: BAS and BFRS Compliance analysis of Square Pharmaceutical Limited using the applicable financial reporting framework.

Sir,With due respect, we are pleased to submit the term paper that you asked for as a part of our BBA course and we are delighted to inform you that we have completed the report on BFRS and BAS compliance analysis on Square Pharmaceutical Limited as the partial course requirement of course F-201. We tried our best to work carefully and sincerely to make the report informative.

The study we conducted enhanced our knowledge to make an executive report. This report has given us an exceptional experience that might have immense uses in the future endeavors. We sincerely hope that it would be able to fulfill your expectations.

We have put our sincere effort to give this report a presentable shape and make it as precise as possible. We cordially thank you for providing us with this unique opportunity.

Sincerely yours,

Tasfia Tasneem Ahmed

On behalf of,

Group: 13

Thank You.

3

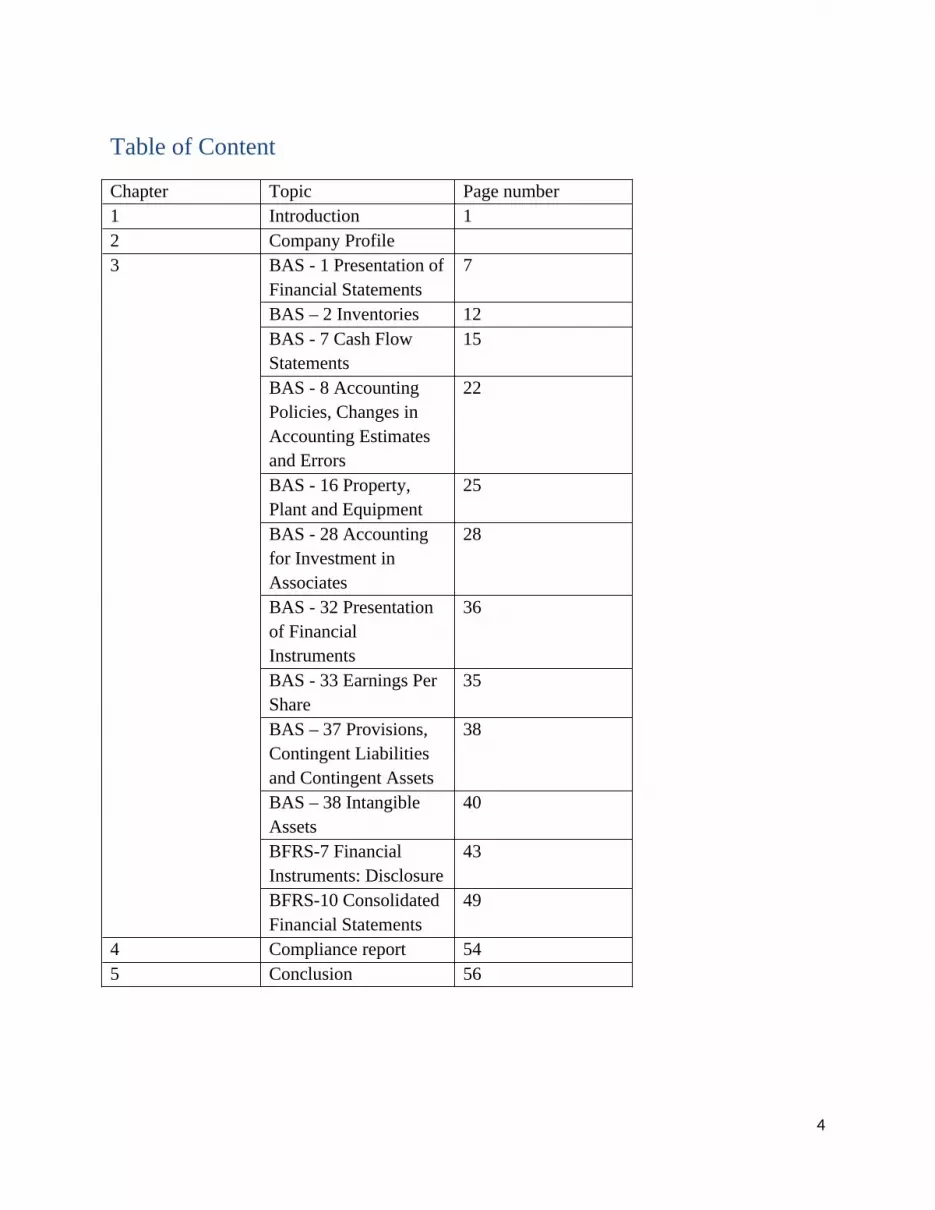

Table of Content

Chapter Topic Page number1 Introduction 12 Company Profile3 BAS - 1 Presentation of

Financial Statements7

BAS – 2 Inventories 12BAS - 7 Cash Flow Statements

15

BAS - 8 Accounting Policies, Changes in Accounting Estimates and Errors

22

BAS - 16 Property, Plant and Equipment

25

BAS - 28 Accounting for Investment in Associates

28

BAS - 32 Presentation of Financial Instruments

36

BAS - 33 Earnings Per Share

35

BAS – 37 Provisions, Contingent Liabilities and Contingent Assets

38

BAS – 38 Intangible Assets

40

BFRS-7 Financial Instruments: Disclosure

43

BFRS-10 Consolidated Financial Statements

49

4 Compliance report 545 Conclusion 56

4

Executive Summary

We were assigned to implement the topic we have learnt throughout our Financial Accounting and Reporting, F-201 course, about the financial statement analysis of a company. This generally refers to the BAS and BFRS standards. So we have chosen Square Pharmaceuticals Limited and conducted our analysis on it. We have tried to cover every standard we have been taught in this course and that is available for public usage about the topic.

1) BFRS 7 which is Financial Instrument: Disclosure.

2) BFRS 10 Group Accounts (Control) We have also analyzed:

1) BAS 1 Presentation of Financial statement 2) BAS 2 Inventories3) BAS 7 Cash Flow Statement4) BAS 8 Accounting Policies, Changes in Accounting Estimates and Errors5) BAS 16 Property, Plant and Equipment6) BAS 28 Investment in Associate7) BAS - 32 Presentation of Financial Instruments 8) BAS 33 EPS9) BAS 37 Provision & Contingencies10) BAS 38 Intangible Assets

We have analyzed compliance of Square Pharmaceuticals Ltd with these BFRS and BAS while preparing their financial statement.

Moreover, we have tried to present a theoretical basis along with the implementation of these accounting standards. Thereafter, we have found out the fundamental analysis of these accounting standards.

5

Chapter 1

Introduction

6

Introduction:

The conceptual framework is a recent concept. In fact, many accounting standard setters have historically operated without having a conceptual framework in place. This resulted in accounting standards often being haphazard in nature and largely a response to the issues or scandals of the day – reactive rather than proactive. The lack of an agreed conceptual framework also increases the risk that standards are inconsistent with each other and that there is no overall objective for the preparation of financial statements.

A statement of the functions of financial statements included in a framework document increases the robustness of the standard-setting process, ensures consistency and assists in the development of future standards. The framework can assist users in interpreting information contained within financial statements as it provides an understanding of the principles on which they are prepared. Each national standard-setting body has its own conceptual framework providing the foundations on which its accounting standards are based. For Bangladesh such standard setting bodies Bangladesh Accounting Standards (BAS) and Bangladesh Financial Reporting Standards (BFRS). Companies that prepare financial statements follow the BAS and BFRS framework

This report is prepared on the basis of “Compliance of the rules & regulations of BAS (Bangladesh Accounting Standard) in preparing the financial statements of Square Pharmaceuticals Limited.

Objective of the study:

The main objective of the study was to

1. Know how a company uses the frameworks of BAS and BFRS to prepare their financial statement.

2. Compare the similarities and dissimilarities among the company’s policy and the frameworks of BFRS and BAS.

Scope of the study:

This study has given us a brainstorming session. It has also given us the opportunity to apply the theoretical knowledge in solving a practical problem.

Methodology:

Area of Investigation:We have investigated the Financial Statement of Square Pharmaceuticals Limited.

Source of Information:

7

Secondary: We have used data collected from DSC, our text book and other secondary sources of information.

LIMITATIONS:

As we are just the beginners of learning this course the followings were our limitations

Lack of experience in this field Lack of depth of knowledge Getting the information and interpreting it, on the basis of our understanding and then

implementing it.

8

Chapter 2

Company Profile

9

Company Profile

Square Pharmaceutical Limited was incorporated on 10 November 1964 under the Companies Act 1913 as a Private Ltd. Company and it was converted into a Public Limited Company in 1991 and offered its share to the public with the approval of the Bangladesh Securities and Exchange Commission in the month of December 1994. The shares of the company are listed in the Dhaka Stock Exchange Ltd. and Chittagong Stock Exchange Ltd.

Vision:

They view the business as a means to the material and social wellbeing of the investors, employees and the society at large leading to accretion of wealth through financial and moral gains as a part of the processof the human civilization.

Mission:

Their Mission is to produce and provide quality & innovative healthcare relief for people, maintain stringently ethical standard in business operation also ensuring benefit to the shareholders, stakeholders and the society at large.

Objective:

Their objectives are to conduct transparent business operation based on market mechanism within the legal & social frame work with aims to attain the mission reflected by our vision.

Corporate Focus:

Their vision, mission and objectives are to emphasis on the quality of product, process and services leading to growth of the company imbibed with good governance practices.

10

Chapter: 3

Application Of

BAS and BFRS Framework

11

BAS 1Presentation of Financial Statements

Theoretical Overview What information financial statements provide?Financial statements provide information about-

Financial Position Financial Statements Cash flow Statements

Objective

BAS 1(presentation of financial statements) prescribes the basis for the presentation for financial statements, so as to ensure comparability with:

The entity’s own financial statement of previous periods; and The Financial statement of other companies.

BAS 1 must be applied to all general purpose financial statements prepared in accordance with BFRS. BAS 1 is concerned with overall considerations about the minimum content of a set of financial statements.

Purpose

The objective of general purpose financial statements is to provide information about-

Financial position Financial performance and cash flow Management stewardship

In order to achieve this, information is provided about the following aspects of the entity’s results:

Assets Liabilities Equity Income and expenses Other changes in equity Cash flows

12

BAS 1 requires that they should be clearly identified and distinguished from other information presented.

Structure and content

Balance sheet

The following guidelines are given in BAS 1 about the presentation of balance sheet.

BAS 1 provides guidance on the layout of the balance sheet. BAS 1 specifies that certain items must be shown on the face of the balance sheet. Other information is required on the face of the balance sheet or in the notes. Both assets and liabilities must be separately classified as current and non-current.

Income Statement

The following guidelines are given in BAS 1 about the presentation of income statement. BAS 1 suggests two formats for the income statement BAS 1 specifies that certain items must be shown on the face of the income statement Other information is required on the face of the income statement or in the notes

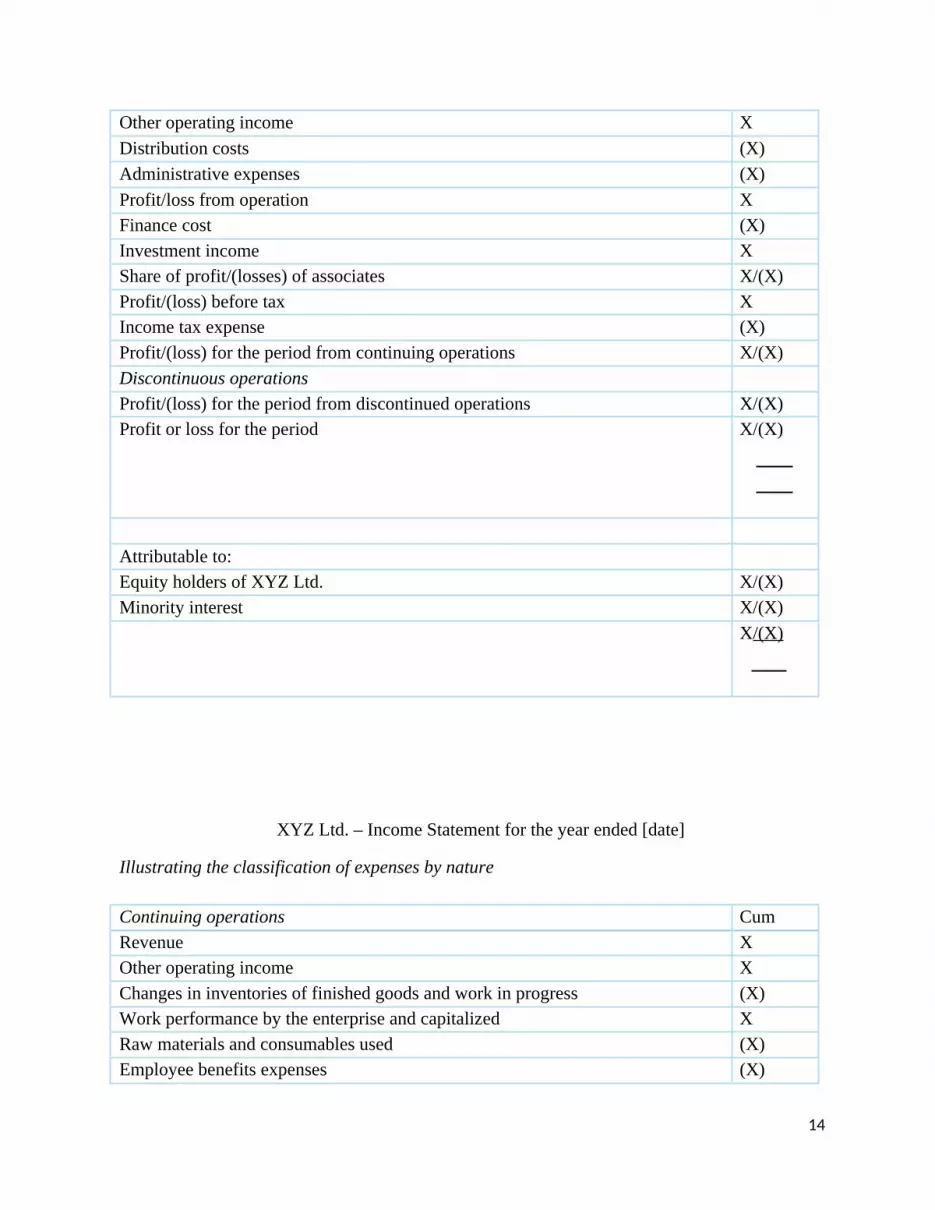

Income statement formats:

BAS 1 suggests two possible formats for the income statement, the different between them being the classification of expenses:

By function, or By nature

These two formats are given visualized bellow to show the example of format of income statement that is created by companies complied BAS 1

XYZ Ltd. – Income Statement for the year ended [date]

Illustrating the classification of expenses by function

Continuing operations CumRevenue XCost of sales (X)Gross profit X

13

Other operating income XDistribution costs (X)Administrative expenses (X)Profit/loss from operation XFinance cost (X)Investment income XShare of profit/(losses) of associates X/(X)Profit/(loss) before tax XIncome tax expense (X)Profit/(loss) for the period from continuing operations X/(X)Discontinuous operationsProfit/(loss) for the period from discontinued operations X/(X)Profit or loss for the period X/(X)

Attributable to:Equity holders of XYZ Ltd. X/(X)Minority interest X/(X)

X/(X)

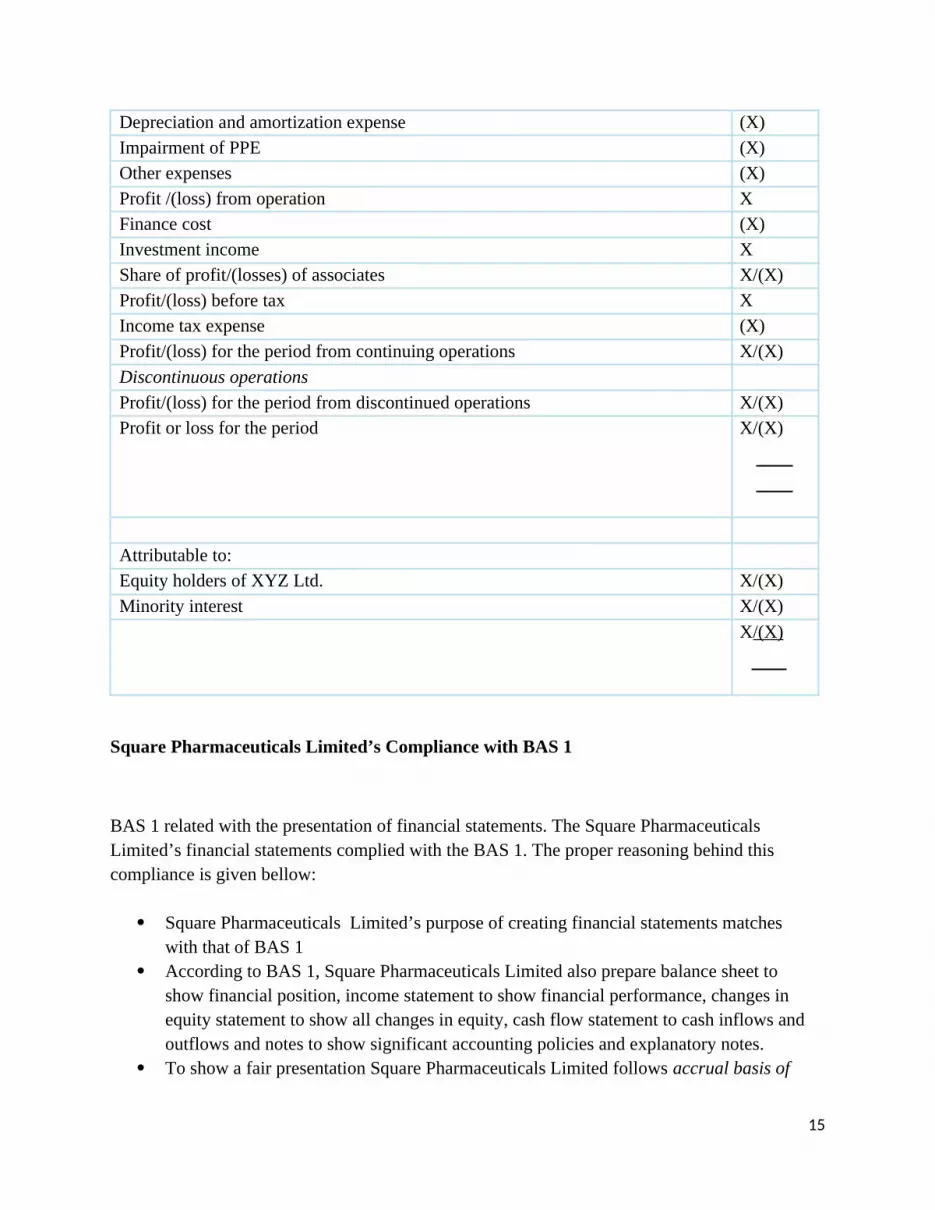

XYZ Ltd. – Income Statement for the year ended [date]

Illustrating the classification of expenses by nature

Continuing operations CumRevenue XOther operating income XChanges in inventories of finished goods and work in progress (X)Work performance by the enterprise and capitalized XRaw materials and consumables used (X)Employee benefits expenses (X)

14

Depreciation and amortization expense (X)Impairment of PPE (X)Other expenses (X)Profit /(loss) from operation XFinance cost (X)Investment income XShare of profit/(losses) of associates X/(X)Profit/(loss) before tax XIncome tax expense (X)Profit/(loss) for the period from continuing operations X/(X)Discontinuous operationsProfit/(loss) for the period from discontinued operations X/(X)Profit or loss for the period X/(X)

Attributable to:Equity holders of XYZ Ltd. X/(X)Minority interest X/(X)

X/(X)

Square Pharmaceuticals Limited’s Compliance with BAS 1

BAS 1 related with the presentation of financial statements. The Square Pharmaceuticals Limited’s financial statements complied with the BAS 1. The proper reasoning behind this compliance is given bellow:

Square Pharmaceuticals Limited’s purpose of creating financial statements matches with that of BAS 1

According to BAS 1, Square Pharmaceuticals Limited also prepare balance sheet to show financial position, income statement to show financial performance, changes in equity statement to show all changes in equity, cash flow statement to cash inflows and outflows and notes to show significant accounting policies and explanatory notes.

To show a fair presentation Square Pharmaceuticals Limited follows accrual basis of

15

accounting and follow going concern basis. Square Pharmaceuticals Limited maintains consistency in accounting as they are using

accrual basis of accounting and going concern basis from the beginning of their inception.

Their financial statements are comparable with relevant previous years as shown in the annual report of 2014-15 where every element of financial statements is compared with previous year 2013-14.

Square Pharmaceuticals Limited’s balance sheet has matched sample of BAS 1 and its elements also has matched with it.

Square Pharmaceuticals Limited’s income statement and cash flow statement are also presented as per BAS 1.

Income statement the Square Pharmaceuticals Limited has followed the format of income statement where the expenses are classified by their functions not by nature.

The presentation of equity statement and Cash flow statement of Square Pharmaceuticals Limited also matched with the given format of BAS 1.

16

BAS-2:Inventories

Theoretical Overview:Objective:BAS 2 discusses about the treatment of inventories. The objective of BAS 2 is to prescribe the accounting treatment for inventories. In particular, it provides guidance on the determination of cost and its subsequent recognition as an expense, including any write-down to net realizable value.Measurement:According to BAS 2, in measuring inventories we should select the lower of cost and net realizable value.Cost should include all:

costs of purchase (including taxes, transport, and handling) net of trade discounts received

costs of conversion (including fixed and variable manufacturing overheads) and other costs incurred in bringing the inventories to their present location and condition

Borrowing Costs identifies some limited circumstances where borrowing costs (interest) can be included in cost of inventories that meet the definition of a qualifying asset. Inventory cost should not include:

abnormal waste storage costs administrative overheads unrelated to production selling costs foreign exchange differences arising directly on the recent acquisition of inventories

invoiced in a foreign currency Interest cost when inventories are purchased with deferred settlement terms.

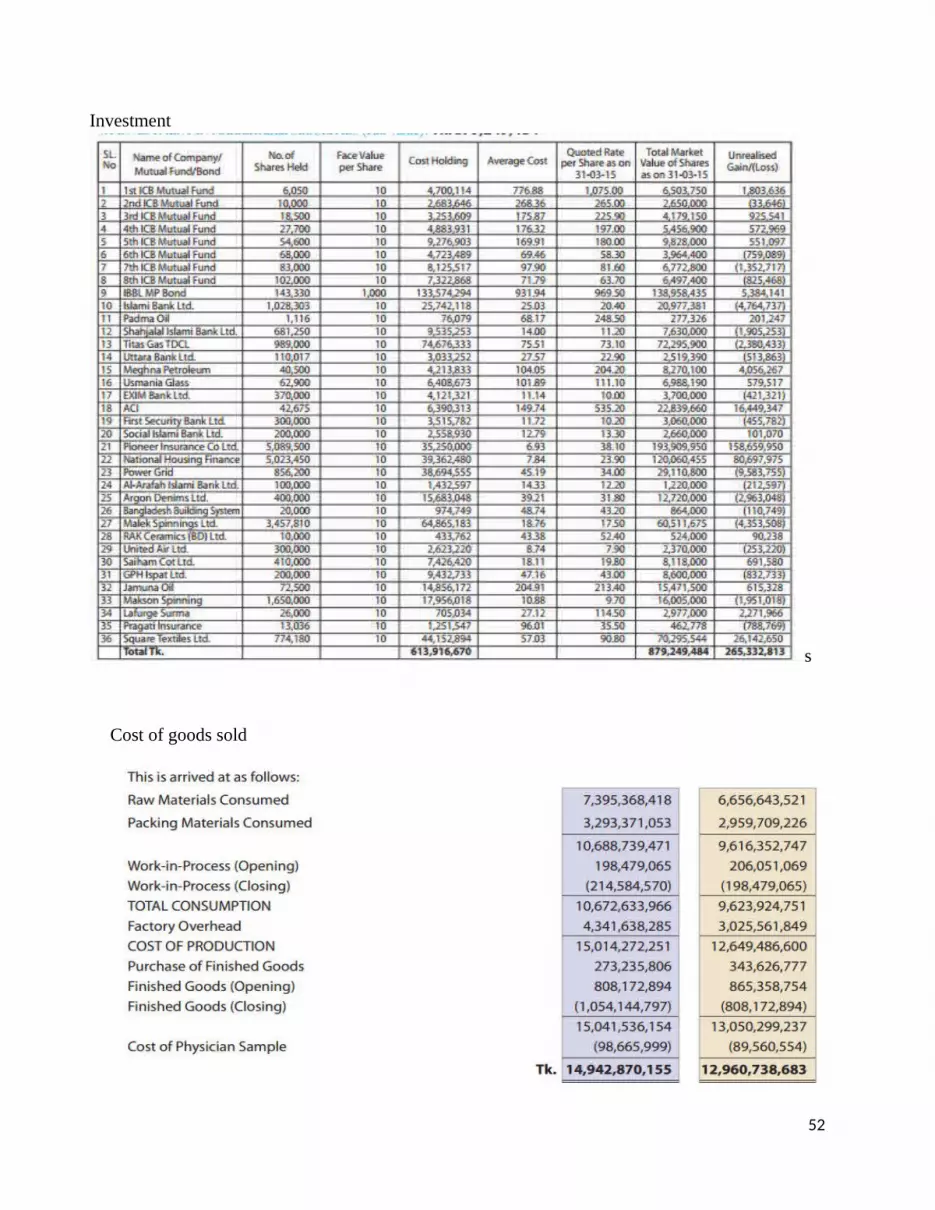

Square Pharmaceuticals Limited’s Compliance with BAS 2:

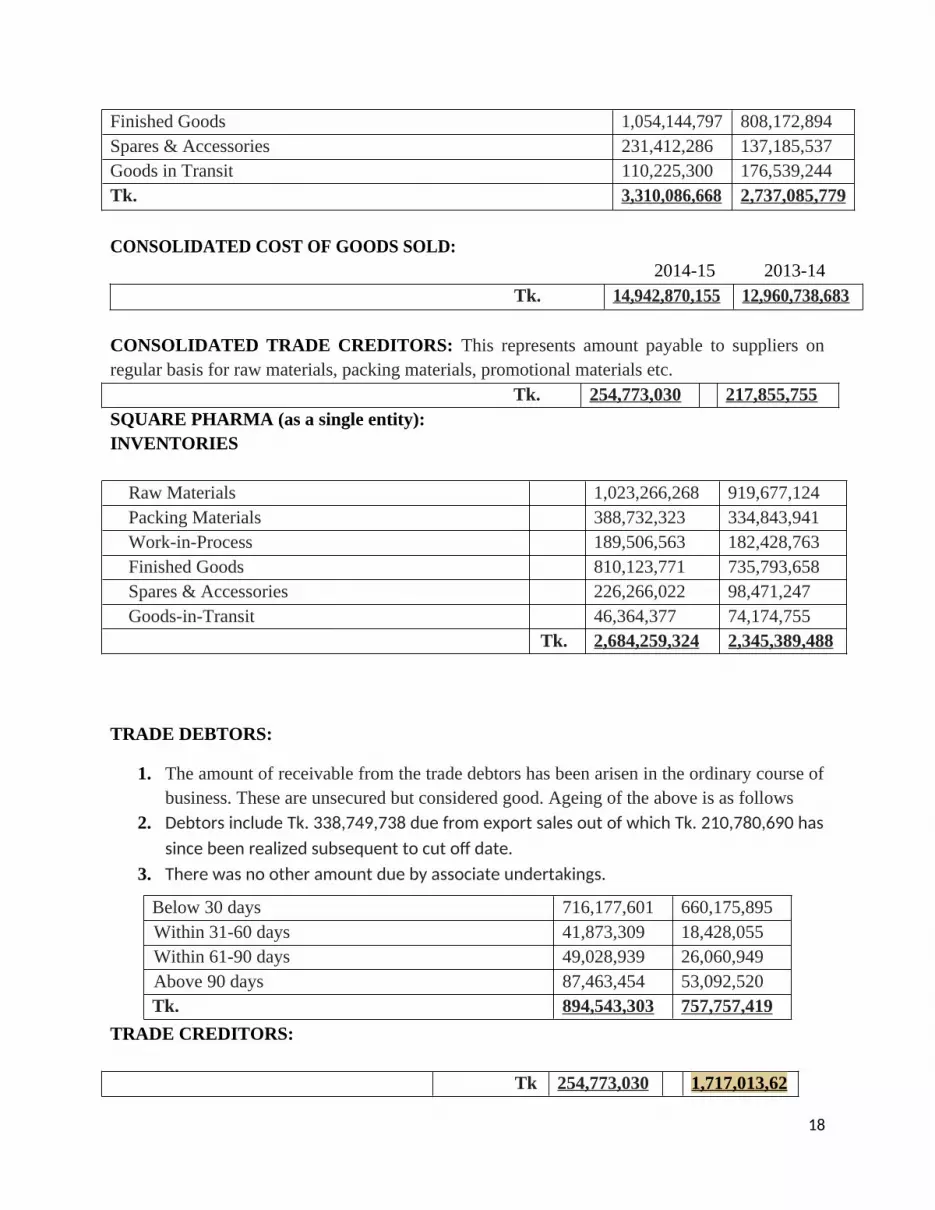

CONSOLIDATED INVENTORIES:

The basis of valuation is stated in Note- 1.10. The break-up is as under:

Raw Materials 1,259,076,254 1,034,811,917Packing Materials 440,643,461 381,897,122Work-in-Process 214,584,570 198,479,065

17

Finished Goods 1,054,144,797 808,172,894Spares & Accessories 231,412,286 137,185,537Goods in Transit 110,225,300 176,539,244Tk. 3,310,086,668 2,737,085,779

CONSOLIDATED COST OF GOODS SOLD: 2014-15 2013-14

Tk. 14,942,870,155 12,960,738,683

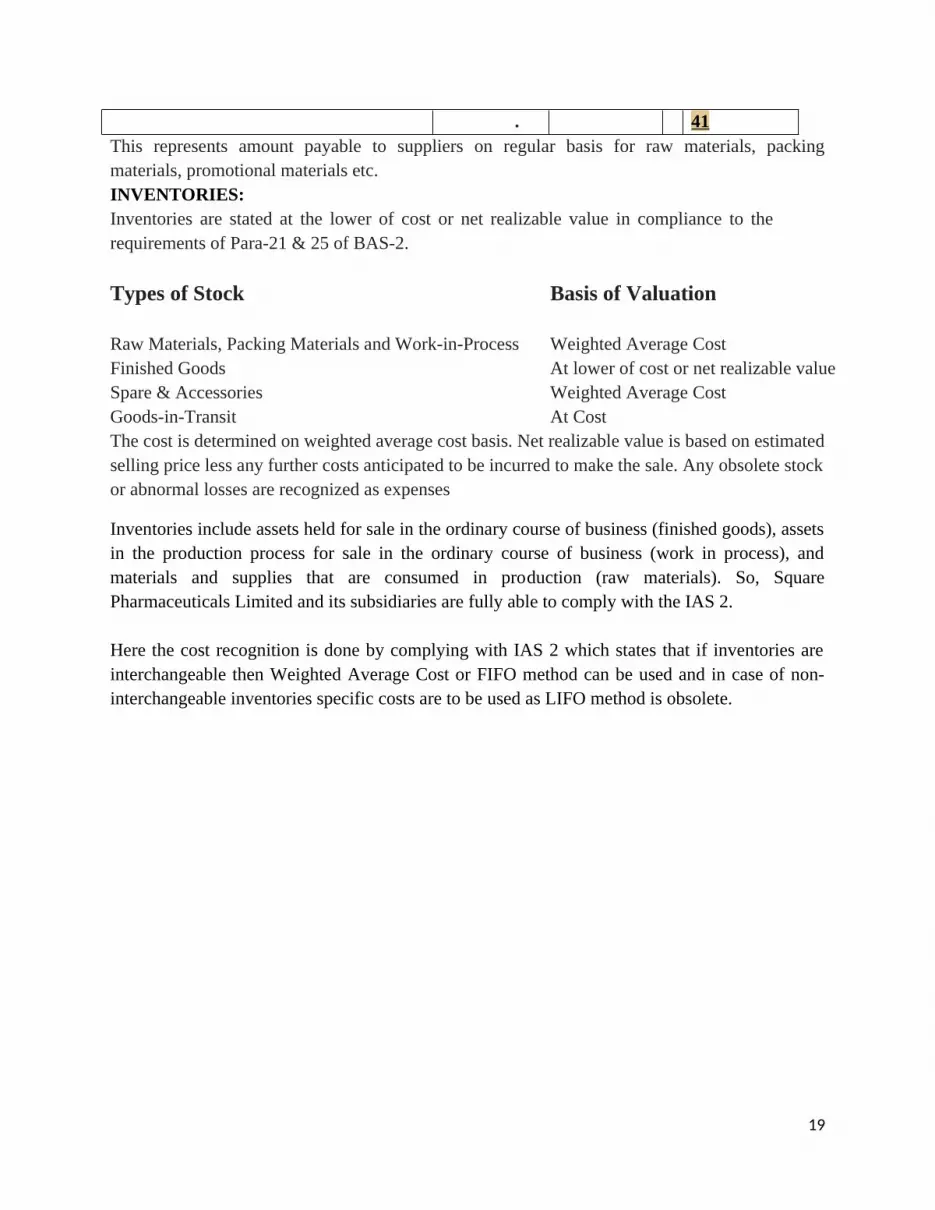

CONSOLIDATED TRADE CREDITORS: This represents amount payable to suppliers on regular basis for raw materials, packing materials, promotional materials etc.

Tk. 254,773,030 217,855,755SQUARE PHARMA (as a single entity): INVENTORIES

Raw Materials 1,023,266,268 919,677,124Packing Materials 388,732,323 334,843,941Work-in-Process 189,506,563 182,428,763Finished Goods 810,123,771 735,793,658Spares & Accessories 226,266,022 98,471,247Goods-in-Transit 46,364,377 74,174,755

Tk. 2,684,259,324 2,345,389,488

TRADE DEBTORS:

1. The amount of receivable from the trade debtors has been arisen in the ordinary course of business. These are unsecured but considered good. Ageing of the above is as follows

2. Debtors include Tk. 338,749,738 due from export sales out of which Tk. 210,780,690 has since been realized subsequent to cut off date.

3. There was no other amount due by associate undertakings.

TRADE CREDITORS:

Tk 254,773,030 1,717,013,62

18

Below 30 days 716,177,601 660,175,895Within 31-60 days 41,873,309 18,428,055Within 61-90 days 49,028,939 26,060,949Above 90 days 87,463,454 53,092,520Tk. 894,543,303 757,757,419

. 41This represents amount payable to suppliers on regular basis for raw materials, packing materials, promotional materials etc.INVENTORIES:Inventories are stated at the lower of cost or net realizable value in compliance to the requirements of Para-21 & 25 of BAS-2.

Types of Stock Basis of Valuation

Raw Materials, Packing Materials and Work-in-Process Weighted Average CostFinished Goods At lower of cost or net realizable valueSpare & Accessories Weighted Average CostGoods-in-Transit At CostThe cost is determined on weighted average cost basis. Net realizable value is based on estimated selling price less any further costs anticipated to be incurred to make the sale. Any obsolete stock or abnormal losses are recognized as expenses

Inventories include assets held for sale in the ordinary course of business (finished goods), assets in the production process for sale in the ordinary course of business (work in process), and materials and supplies that are consumed in production (raw materials). So, Square Pharmaceuticals Limited and its subsidiaries are fully able to comply with the IAS 2.

Here the cost recognition is done by complying with IAS 2 which states that if inventories are interchangeable then Weighted Average Cost or FIFO method can be used and in case of non-interchangeable inventories specific costs are to be used as LIFO method is obsolete.

19

BAS 7

Cash Flow Statements

Theoretical Overview:

A cash flow statement is a financial report that describes the sources of a company’s cash and how the cash was spent over a specified time period. It does not include non-cash item such as depreciation.

Objective:

The objective of BAS 7 Cash flow statement is to provide historical information about changes in cash and cash equivalent, classifying cash flows between operating, investing, and financingactivities. This will provide information to users of financial statements about the entity’s ability to generate cash and cash equivalents, as indicating the cash needs of the entity.

Cash:Cash comprises cash on hand and demand deposit.

Cash equivalent: Short-term, highly liquid investments that are readily convertible to knownamounts of cash and which are subject to an insignificant risk of change in value.

Scope:

A cash flow statement should be presented as an integral part of an entity’s financial statements.

All types of entities are required by the standard to produce a cash flow statement.

Presentation

BAS 7 requires cash flow statements to report cash flows during the period classified by:

Operating activities Investing activities Financing activities i) Operating Activities:

Cash from operating activities usually refers to the net cash inflow reported in the first section of the statement of cash flows. Cash from operating activities focuses on the cash inflows and outflows from a company's main business activities of buying and selling merchandise, providing services, etc.

20

The standard gives the following as example of cash flows from operating activities.

Cash receipts from the sale of goods and the rendering of services.

Cash receipts from royalties, fees, commissions and other revenue.

Cash payments to suppliers for goods and services.

Cash payments to and on behalf of employees.

Cash flows from interest paid and income taxes paid are also dealt with here.

Cash generated from operations:

BAS 7 allows two possible layouts for cash generated from operations

The indirect method

The direct method

The direct method is preferred by BAS 7 but not required. In practical terms the indirect method is likely to be easier and less time consuming to prepare and is more likely to be examined.

Indirect Method:

Using the indirect method, cash generated from operations is calculated by performing reconciliation between:

Profit before tax as reported in the income statement, and

Cash generated from operations.

Direct Method:

Using direct method cash generated from operations would be analyzed as follows and shows as a note to the cash flow statement:

Gross operating cash flows for the year ended 31 December 20X7

Cash receipt from customerCash paid to supplier and employeesCash generated from operations

CU X (X) (X)

21

ii) Investing Activities:

Cash flow from investing activities is an item on the cash flow statement that reports the aggregate change in a company's cash position resulting from any gains (or losses) from investments in the financial markets and operating subsidiaries and changes resulting from amounts spent on investments in capital assets such as plant and equipment.

Purchase of fixed assets (negative cash flow)

Sale of fixed assets (positive cash flow)

Purchase of investment instruments, such as stocks and bonds (negative cash flow)

Sale of investment instruments, such as stocks and bonds (positive cash flow)

Lending of money (negative cash flow) and Collection of loans (positive cash flow)

Cash payment to acquire equity or debt of other entities

Interest received and Dividend received

iii)Financing Activities:

This sections of cash flow statement shows the share of cash which the entity’s capital providers have claimed during the period. This is an indicator of likely future interest and dividend payments. The standard gives the following examples cash flows which might arise under this heading.

Cash proceeds from issuing shares Cash payments to owners to acquire or redeem the entity’s shares Cash proceeds from issuing debentures, loans, notes, bonds, mortgages and other short

and long-term borrowings Repayments of capital of amounts borrowed under finance leases Dividend paidDisclosuresBAS 7 requires certain additional disclosures to accompany the cash flow statement.

Components of cash and cash equivalent: the following disclosures are required:

The components of cash and cash equivalents.

A reconciliation showing the amounts in the cash flow statement reconcile with the equivalent items reported in the balance sheet.

22

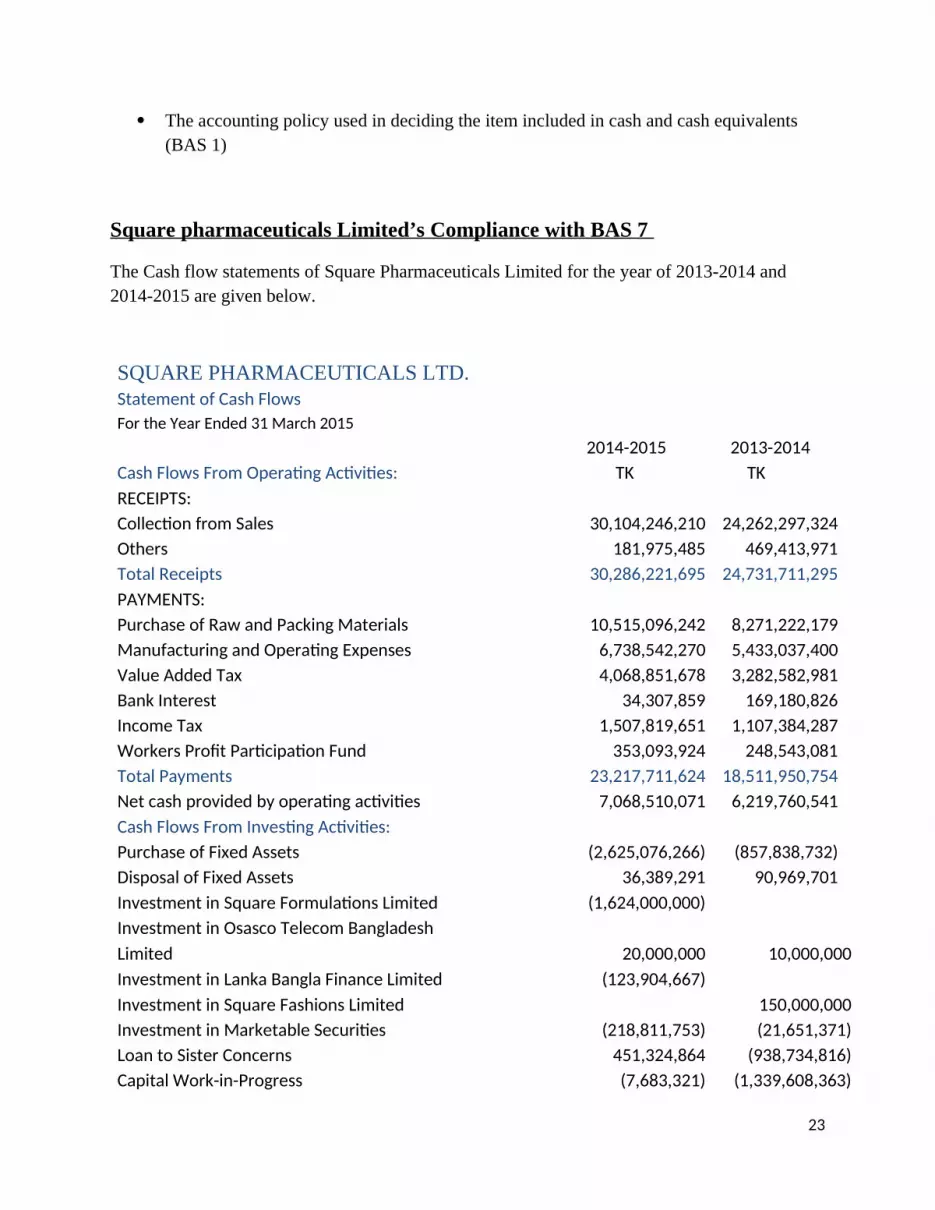

The accounting policy used in deciding the item included in cash and cash equivalents (BAS 1)

Square pharmaceuticals Limited’s Compliance with BAS 7

The Cash flow statements of Square Pharmaceuticals Limited for the year of 2013-2014 and 2014-2015 are given below.

SQUARE PHARMACEUTICALS LTD.Statement of Cash FlowsFor the Year Ended 31 March 2015

2014-2015 2013-2014Cash Flows From Operating Activities: TK TKRECEIPTS:Collection from Sales 30,104,246,210 24,262,297,324Others 181,975,485 469,413,971Total Receipts 30,286,221,695 24,731,711,295PAYMENTS:Purchase of Raw and Packing Materials 10,515,096,242 8,271,222,179Manufacturing and Operating Expenses 6,738,542,270 5,433,037,400Value Added Tax 4,068,851,678 3,282,582,981Bank Interest 34,307,859 169,180,826Income Tax 1,507,819,651 1,107,384,287Workers Profit Participation Fund 353,093,924 248,543,081Total Payments 23,217,711,624 18,511,950,754Net cash provided by operating activities 7,068,510,071 6,219,760,541Cash Flows From Investing Activities:Purchase of Fixed Assets (2,625,076,266) (857,838,732)Disposal of Fixed Assets 36,389,291 90,969,701Investment in Square Formulations Limited (1,624,000,000)Investment in Osasco Telecom Bangladesh Limited 20,000,000 10,000,000Investment in Lanka Bangla Finance Limited (123,904,667)Investment in Square Fashions Limited 150,000,000Investment in Marketable Securities (218,811,753) (21,651,371)Loan to Sister Concerns 451,324,864 (938,734,816)Capital Work-in-Progress (7,683,321) (1,339,608,363)

23

Gain on Sale of Marketable Securities 6,863,121 6,598,771Interest Received 303,803,237 154,859,960Dividend Received 158,561,700 125,399,281Net cash used in investing activities (3,622,533,794) (2,620,005,569)Cash Flows From Financing Activities:Long Term Loan Received 7,514,001Long Term Loan Repaid (182,416,885) (528,423,588)Short Term Bank Loan Repaid (120,920,108.00) (998,056,098)Dividend Paid (1,445,997,789) (926,921,660)Net cash used in financing activities (1,749,334,782) (2,445,887,345)Increase in Cash and Cash Equivalents 1,696,641,495 1,153,867,627Cash and Cash Equivalents at the Opening 2,152,834,279 932,407,871Cash and Cash Equivalents at the Closing 3,849,475,774 2,086,275,498

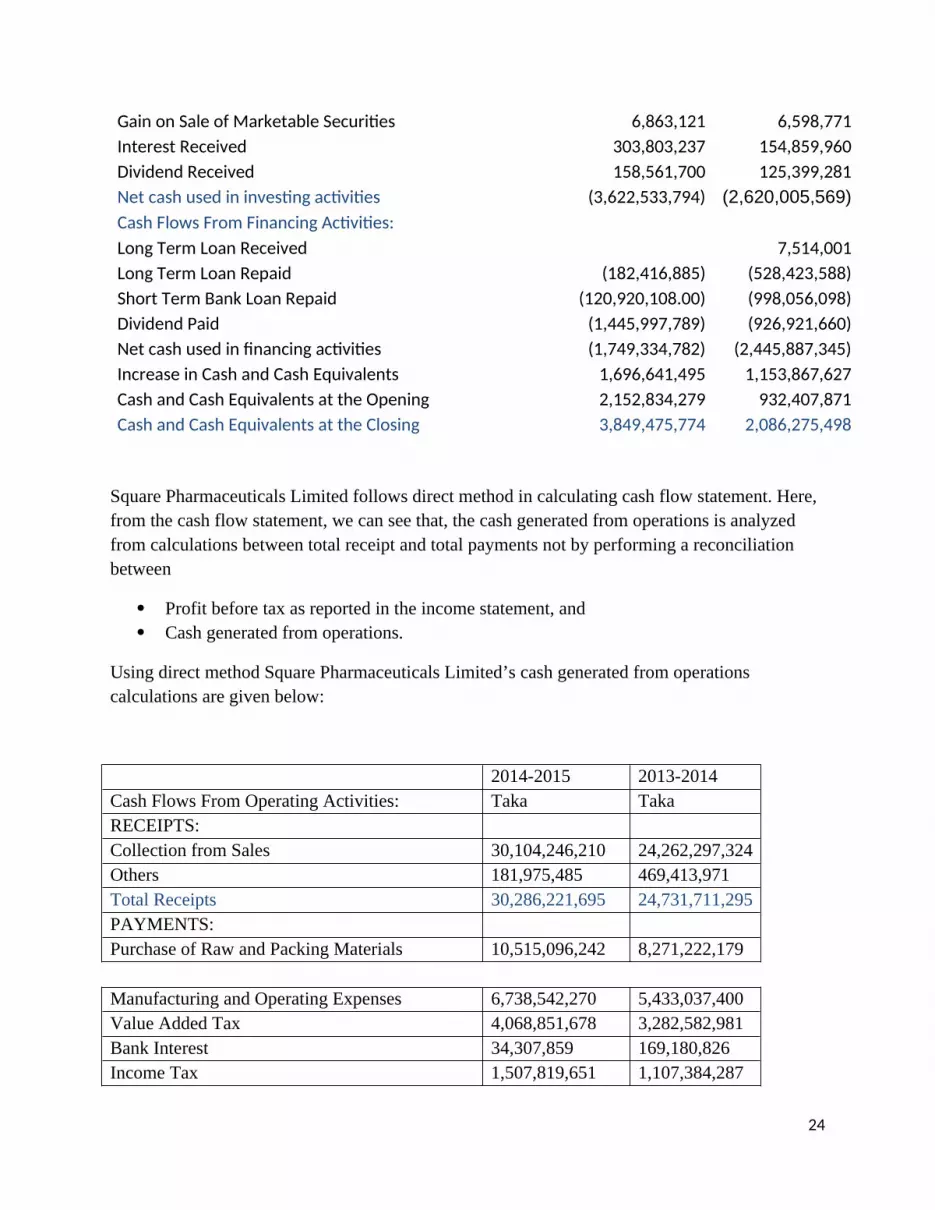

Square Pharmaceuticals Limited follows direct method in calculating cash flow statement. Here, from the cash flow statement, we can see that, the cash generated from operations is analyzed from calculations between total receipt and total payments not by performing a reconciliation between

Profit before tax as reported in the income statement, and Cash generated from operations.

Using direct method Square Pharmaceuticals Limited’s cash generated from operations calculations are given below:

2014-2015 2013-2014Cash Flows From Operating Activities: Taka TakaRECEIPTS:Collection from Sales 30,104,246,210 24,262,297,324Others 181,975,485 469,413,971Total Receipts 30,286,221,695 24,731,711,295PAYMENTS:Purchase of Raw and Packing Materials 10,515,096,242 8,271,222,179

Manufacturing and Operating Expenses 6,738,542,270 5,433,037,400Value Added Tax 4,068,851,678 3,282,582,981Bank Interest 34,307,859 169,180,826Income Tax 1,507,819,651 1,107,384,287

24

Workers Profit Participation Fund 353,093,924 248,543,081Total Payments 23,217,711,624 18,511,950,754Net cash provided by operating activities 7,068,510,071 6,219,760,541

Figure: Cash generated from operations of Square Pharmaceuticals Limited.

The direct method is preferred by BAS 7 and Square Pharmaceuticals Limited follows this standard appropriately.Cash flow statement is prepared in accordance with BAS-7 under direct method and as outlined in the Securities and Exchange Rules 1987.

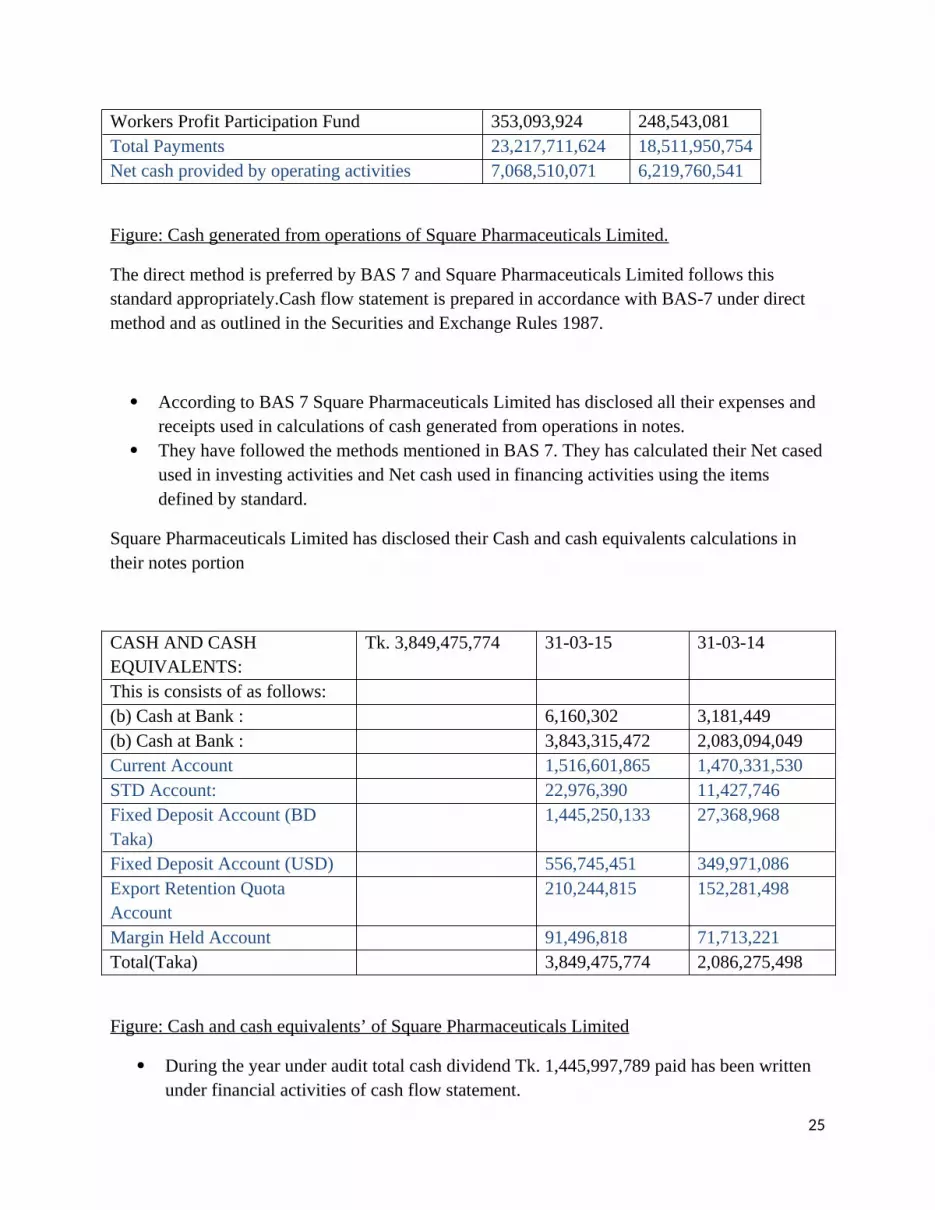

According to BAS 7 Square Pharmaceuticals Limited has disclosed all their expenses and receipts used in calculations of cash generated from operations in notes.

They have followed the methods mentioned in BAS 7. They has calculated their Net cased used in investing activities and Net cash used in financing activities using the items defined by standard.

Square Pharmaceuticals Limited has disclosed their Cash and cash equivalents calculations in their notes portion

CASH AND CASH EQUIVALENTS:

Tk. 3,849,475,774 31-03-15 31-03-14

This is consists of as follows:(b) Cash at Bank : 6,160,302 3,181,449(b) Cash at Bank : 3,843,315,472 2,083,094,049Current Account 1,516,601,865 1,470,331,530STD Account: 22,976,390 11,427,746Fixed Deposit Account (BD Taka)

1,445,250,133 27,368,968

Fixed Deposit Account (USD) 556,745,451 349,971,086Export Retention Quota Account

210,244,815 152,281,498

Margin Held Account 91,496,818 71,713,221Total(Taka) 3,849,475,774 2,086,275,498

Figure: Cash and cash equivalents’ of Square Pharmaceuticals Limited

During the year under audit total cash dividend Tk. 1,445,997,789 paid has been written under financial activities of cash flow statement.

25

Its 150,000 taka investment on Zero Coupon Bond in Lanka Bangla Finance Ltd has been shown under Investment activities in Cash flow statement and other investments also have been disclosed here.

Its dividend received, long term loan repaid and received are also shown under proper head of cash flow statement.

So it can be said they have properly complied with the BAS 7 standard.

26

BAS 8

Accounting policies, Changes in Accounting Estimates & Errors

Introduction:

The objective of BAS 8 Accounting Policies, Changes in Accounting Estimates and Errors is to prescribe the criteria for selecting and changing accounting policies, together with the accounting treatment and disclosure of changes in accounting policies, changes in accounting estimates and correction of errors. This enhances relevance, reliability and comparability. BAS 8 achieves this objective by ensuring that:

Information is available about the accounting policies adopted by different entities. Different entities adopt a common approach to the distinction between a change in

accounting policy and accounting estimates. The scope for accounting policy changes is constrained. Changes in accounting policies, changes in accounting estimates and correction of errors

are dealt with in a comparable manner by different entities.

Accounting Policies:

The specific principles, bases, conventions, rules and practices applied by an entity in preparing and presenting financial statements.

Accounting policies are normally developed by reference to the applicable BFRS or Interpretation together with any relevant implementation guidance issued by the ISAB. Where there is no applicable BFRS or Interpretation management should use its judgment in developing an accounting policy ensuring that the resulting information is relevant and reliable.

Consistency of Accounting Policies:

Once selected, accounting policies should be applied consistently for similar transaction, other events and conditions. The exception to this is where a BFRS requires or allows categorization of items where different policies may be applied to each category.

Changes in accounting Policies:

The same accounting policies are usually adopted from period to period, to enhance comparability thereby allowing users to analyze trends over time in profits, cash flows and financial position. Changes in accounting policy will therefore be rare and should only be made if the change

Is required by a BAS or a BFRS (or an interpretation of a BAS or BFRS)

27

Will result in a more appropriate presentation of events or transactions in the financial statements of the entity(a voluntary change)

Adoption of a new BFRS:

Where a new BFRS is adopted, BAS 8 requires any transitional provisions in the new BFRS itself to be followed. If none are given in the BFRS which is being adopted, then the entity should follow the general principles of BAS 8.

Disclosure:

Certain disclosures are required when a change in accounting policy has a material effect on the current period or any prior period presented, or when it may have a material effect in subsequent periods.

Nature of the change Reasons for the change (why more reliable or relevant) Amount of adjustment for the current period and for each prior period presented for each

line item The fact that comparative information has been restated or that it is impracticable to do

so.

Changes in Accounting Estimates:

An adjustment of the carrying amount of an asset or a liability or the amount of the periodic consumption of an asset, that results from the assessment of the present status of, and expected future benefits and obligations associated with, assets and liabilities. Changes in accounting estimates result from new information or new developments and, accordingly, are not correction of errors. Here are some examples of accounting estimates:

A necessary bad debt allowance Useful lives of depreciable assets Adjustment for obsolescence of inventory

Prior Period Errors:

Period prior errors are omissions from, and misstatements in , the entity’s financial statements for one or more prior periods arising from a failure to use, or misuse of, reliable information that:

Was available when financial statements for those periods were authorized for issue Could reasonably be expected to have been obtained and taken into account in the

preparation and presentation of those financial statements.

28

Such errors include the effects of mathematical mistakes, mistakes in applying policies, oversights or misinterpretations of facts, and fraud.

Square Pharmaceuticals Limited’s Compliance with BAS 8:

Specific accounting policies were selected and applied by the company’s management for significant transactions and events that have material effects. The previous years’ figures were presented according to the same accounting principles. Compared to the previous year, there were no significant changes in the accounting and valuation principles affecting the financial position and performance of the company. Accounting and valuation methods are disclosed for the purpose of clarity.

29

BAS 16: Property, Plant & Equipment

Definition:

Property, plant & equipment are tangible assets held by an entity for more than one accounting period for use in production or supply of goods or services, for rental to others, or for administrative purposes.

Recognition:

An item of property, plant & equipment should be recognized as an asset when:

It is probable that future economic benefits associated with the asset will flow to the entity; and

The cost of the asset can be measured reliably.

Initial Measurement:

An item of property, plant & equipment should initially be measured at its cost:

Include all costs involved in bringing the asset into working condition Include in this initial cost capital costs such as the cost of site preparation, delivery costs,

installation costs Revenue cost should be written off as incurred

Subsequent Expenditure:

Subsequent expenditure on property, plant & equipment should only be capitalized if:

It enhances the economic benefits provided by the asset It relates to an overhaul or required major inspection of the asset It is replacing a component of a complex asset.

Depreciation:

Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life.

Depreciable amount is the cost of an asset or other amount substituted for cost in the financial statements, less its residual value.

Depreciation must be charged from the date it is available for use, that is it is capable of operating in the manner intended by management.

Depreciation Methods:

30

The depreciation method used should present as fairly as possible the pattern in which the asset’s economic benefits are consumed by the entity. Possible methods include:

Straight line Reducing balance Machine hours

A change from one method of providing depreciation to another is permissible only on the ground that:

The new method will give a fairer presentation of the results and of the financial position Does not constitute a change of accounting policy Is a change in accounting estimate.

The carrying amount should be written off over the remaining useful life, commencing with the period in which the change is made.

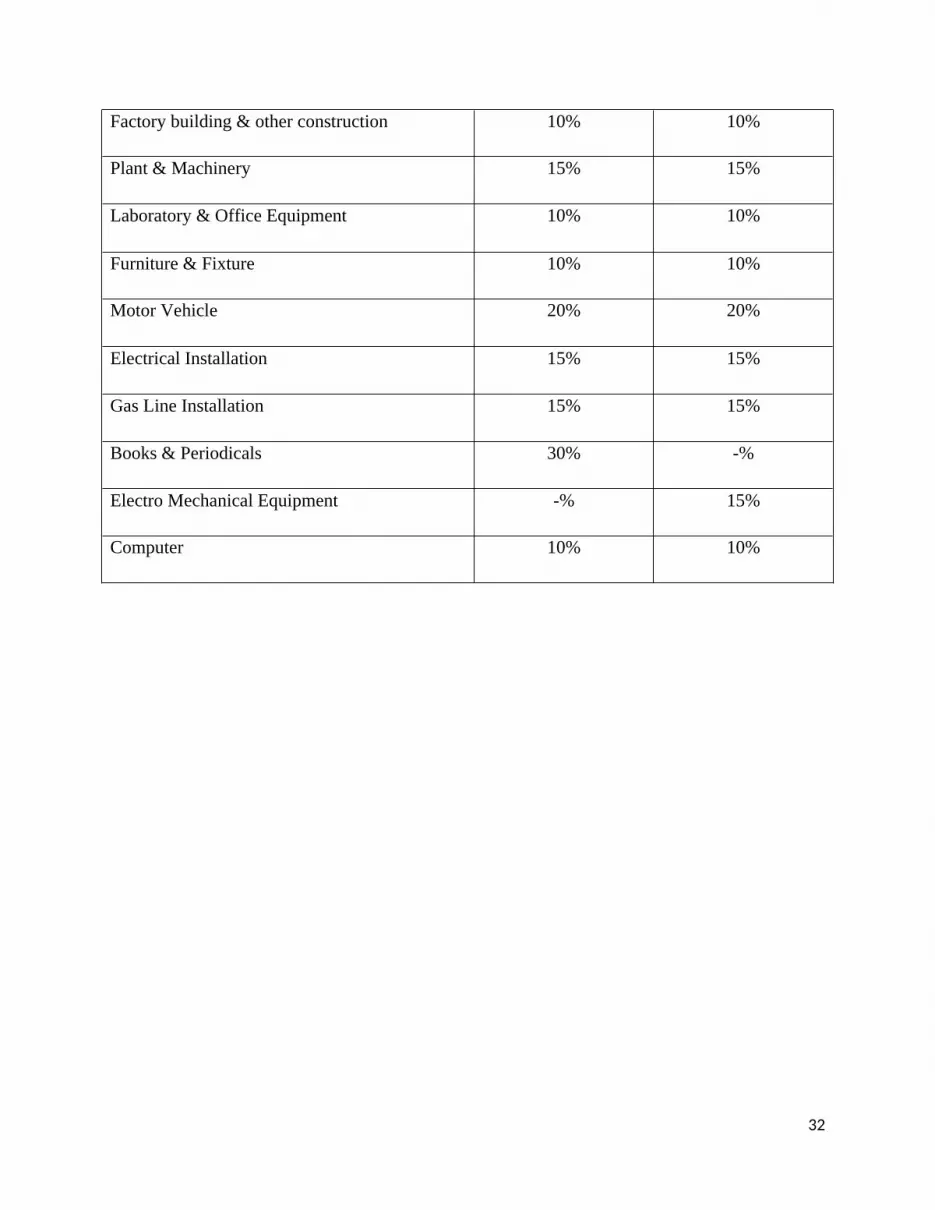

Square Pharmaceuticals Limited’s Compliance with BAS 16:

Square Pharmaceutical LTD accounts for all property, plant & equipment initially at cost and depreciates over their useful life in accordance with BAS-16. The cost of acquisition of an asset comprises its purchase price and any directly attributable cost of bringing the asset into its working condition for its intended use inclusive of inward freight, duties and non-refundable taxes. In respect of major projects involving construction, related pre-operational expenses form part of the value of the asset capitalized. Expenses capitalized also include applicable borrowing cost.

On retirement or other disposal of fixed assets, the cost and accumulated depreciation are eliminated and gain or loss on such disposal is reflected in the income statement which is determined with reference to the net book value of the assets and the net sales proceeds.

Depreciation:

No depreciation is charged on freehold land and on Capital Work-in-Progress. Depreciation is charged on all other fixed assets on a reducing balance method for Square Pharmaceuticals Ltd. (SPL) and Square Formulations Ltd, (SFrL). Depreciation on an asset begins when it is available for use i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by the management.

The rates at which assets are depreciated per annum, depending on the nature and estimated useful life of assets are given below:

Name of assets SPL SFrL

31

Factory building & other construction 10% 10%

Plant & Machinery 15% 15%

Laboratory & Office Equipment 10% 10%

Furniture & Fixture 10% 10%

Motor Vehicle 20% 20%

Electrical Installation 15% 15%

Gas Line Installation 15% 15%

Books & Periodicals 30% -%

Electro Mechanical Equipment -% 15%

Computer 10% 10%

32

BAS 28

Investments in Associates

Theoretical overview

Investments in Associates and Joint Ventures outline how to apply, with certain limited exceptions, the equity method to investments in associates and joint ventures. The standard also defines an associate by reference to the concept of "significant influence", which requires power to participate in financial and operating policy decisions of an investee (but not joint control or control of those polices).

Objective of IAS 28

The objective of IAS 28 (as amended in 2011) is to prescribe the accounting for investments in associates and to set out the requirements for the application of the equity method when accounting for investments in associates and joint ventures.

Significant influence

Where an entity holds 20% or more of the voting power (directly or through subsidiaries) on an investee, it will be presumed the investor has significant influence unless it can be clearly demonstrated that this is not the case. If the holding is less than 20%, the entity will be presumed not to have significant influence unless such influence can be clearly demonstrated. A substantial or majority ownership by another investor does not necessarily preclude an entity from having significant influence

The existence of significant influence by an entity is usually evidenced in one or more of the following ways

• Representation on the board of directors or equivalent governing body of the investee;

• Participation in the policy-making process, including participation in decisions about dividends or other distributions;

• Material transactions between the entity and the investee;

• Interchange of managerial personnel;

• Provision of essential technical information

33

The existence and effect of potential voting rights that are currently exercisable or convertible, including potential voting rights held by other entities, are considered when assessing whether an entity has significant influence. In assessing whether potential voting rights contribute to significant influence, the entity examines all facts and circumstances that affect potential rights

An entity loses significant influence over an investee when it loses the power to participate in the financial and operating policy decisions of that investee. The loss of significant influence can occur with or without a change in absolute or relative ownership levels. [IAS 28(2011).9]

The equity method of accounting

Basic principle:

Under the equity method, on initial recognition the investment in an associate or a joint venture is recognized at cost and the carrying amount is increased or decreased to recognize the investor's share of the profit or loss of the investee after the date of acquisition.

Distributions and other adjustments to carrying amount:

The investor's share of the investee's profit or loss is recognized in the investor's profit or loss. Distributions received from an investee reduce the carrying amount of the investment. Adjustments to the carrying amount may also be necessary for changes in the investor's proportionate interest in the investee arising from changes in the investee's other comprehensive income (e.g. to account for changes arising from revaluations of property, plant and equipment and foreign currency translations.)

Potential voting rights:

An entity's interest in an associate or a joint venture is determined solely on the basis of existing ownership interests and, generally, does not reflect the possible exercise or conversion of potential voting rights and other derivative instruments.

Square Pharmaceuticals Limited’s Compliance with BAS 28

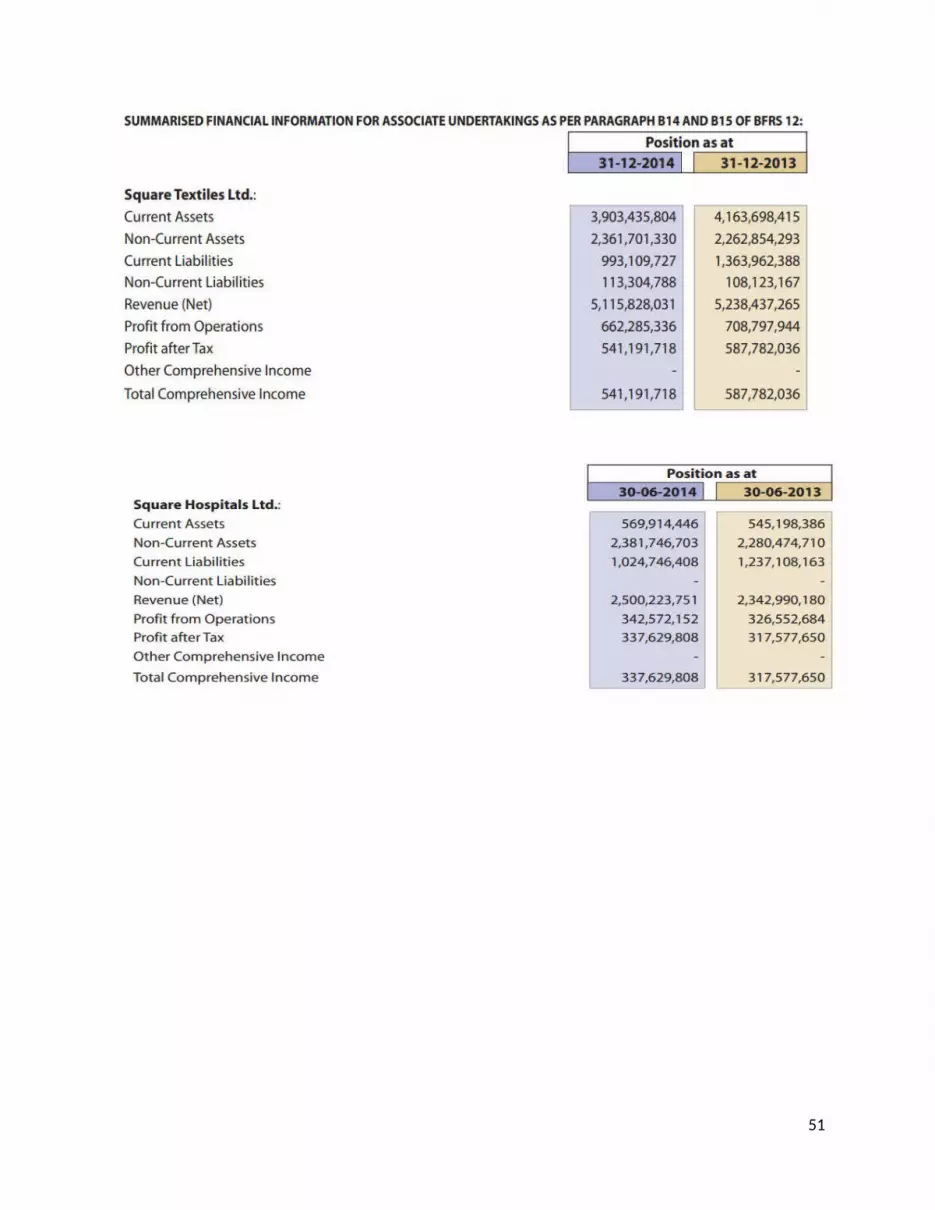

Square Pharmaceuticals Limited has Three Associates.It has followed the equity method of accounting according to the BAS 28 by these steps:

Investment in associate is accounted for in consolidated financial statements under the equity method.

Under the equity method, the investment is initially recorded at cost and the carrying amount is increased or decreased to recognize the investor’s share of the profits or losses of the investee after the date of acquisition. Distributions received from an investee reduce the carrying amount of the investment.

The extract from Notes section:

34

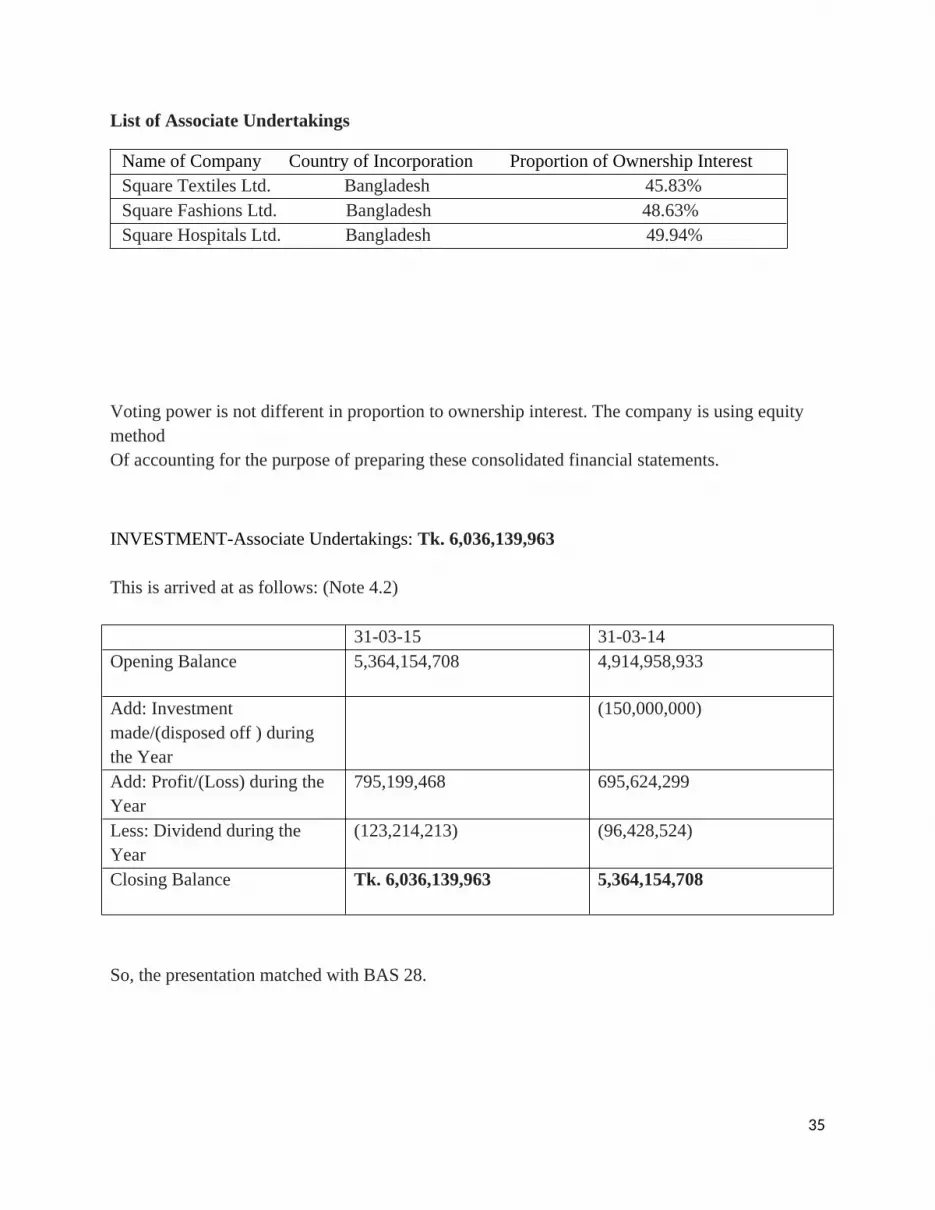

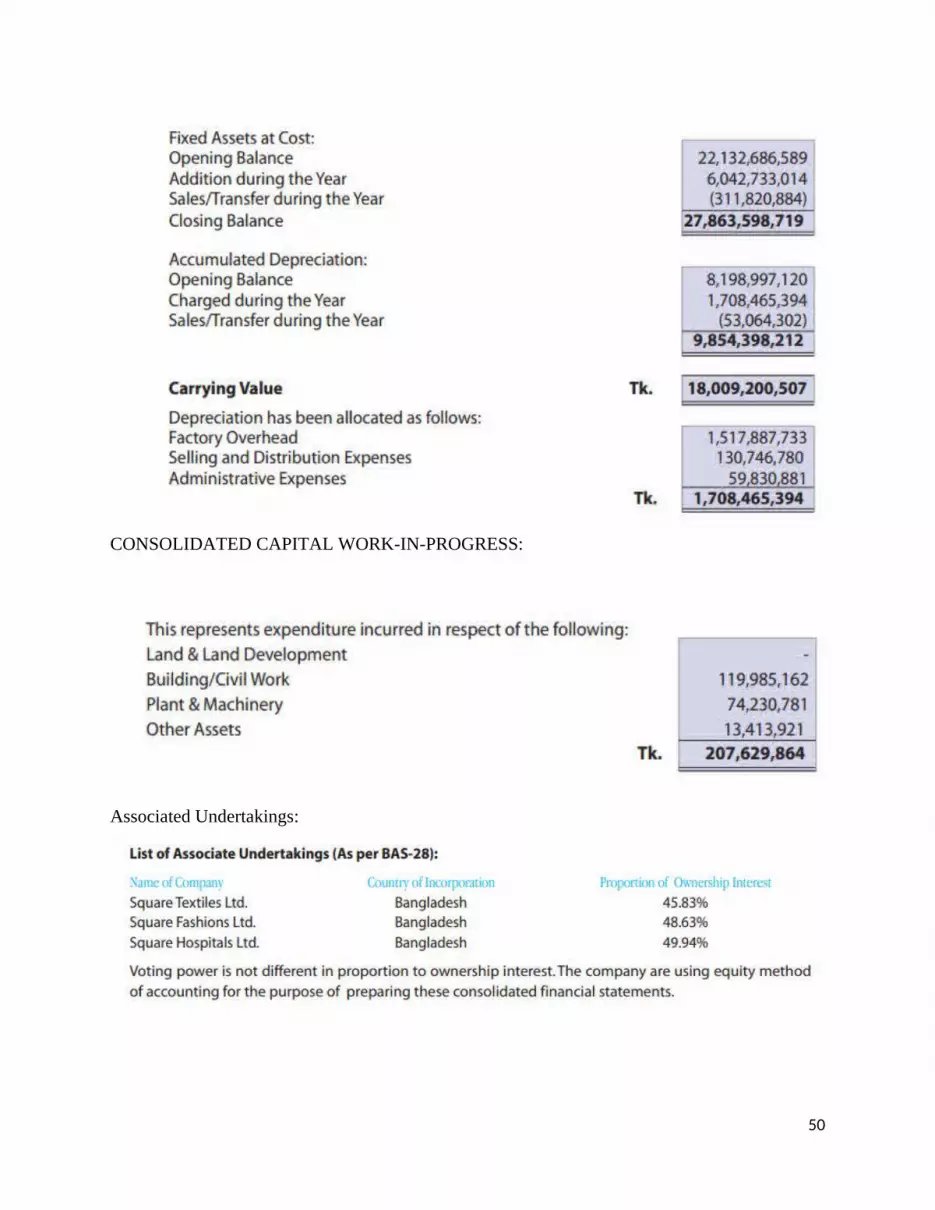

List of Associate Undertakings

Name of Company Country of Incorporation Proportion of Ownership InterestSquare Textiles Ltd. Bangladesh 45.83%Square Fashions Ltd. Bangladesh 48.63%Square Hospitals Ltd. Bangladesh 49.94%

Voting power is not different in proportion to ownership interest. The company is using equity methodOf accounting for the purpose of preparing these consolidated financial statements.

INVESTMENT-Associate Undertakings: Tk. 6,036,139,963

This is arrived at as follows: (Note 4.2)

31-03-15 31-03-14Opening Balance 5,364,154,708 4,914,958,933

Add: Investment made/(disposed off ) during the Year

(150,000,000)

Add: Profit/(Loss) during the Year

795,199,468 695,624,299

Less: Dividend during the Year

(123,214,213) (96,428,524)

Closing Balance Tk. 6,036,139,963 5,364,154,708

So, the presentation matched with BAS 28.

35

BAS 32

Presentation of Financial Instruments

The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity and for offsetting financial assets and liabilities.

IAS 32 addresses this in a number of ways:

clarifying the classification of a financial instrument issued by an entity as a liability or as equity

prescribing the accounting for treasury shares (an entity's own repurchased shares) prescribing strict conditions under which assets and liabilities may be offset in the

balance sheet

Key definitions

Financial instrument: a contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

Financial asset: any asset that is:

cash

an equity instrument of another entity

a contractual right

o to receive cash or another financial asset from another entity; or

o to exchange financial assets or financial liabilities with another entity under conditions that are potentially favorable to the entity; or

a contract that will or may be settled in the entity's own equity instruments and is:

o a non-derivative for which the entity is or may be obliged to receive a variable number of the entity's own equity instruments

o a derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity's own equity instruments. For this purpose the entity's own equity instruments do not include instruments that are themselves contracts for the future receipt or delivery of the entity's own equity instruments

36

o puttable instruments classified as equity or certain liabilities arising on liquidation classified by IAS 32 as equity instruments

Financial liability: any liability that is:

a contractual obligation:

o to deliver cash or another financial asset to another entity; or

o to exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavorable to the entity; or

a contract that will or may be settled in the entity's own equity instruments and isa non-derivative for which the entity is or may be obliged to deliver a variable number of the entity's own equity instruments or

a derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity's own equity instruments. For this purpose the entity's own equity instruments do not include: instruments that are themselves contracts for the future receipt or delivery of the entity's own equity instruments; puttable instruments classified as equity or certain liabilities arising on liquidation classified by IAS 32 as equity instruments

Equity instrument: Any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities.

Fair value: The amount for which an asset could be exchanged or a liability settled, between knowledgeable, willing parties in an arm's length transaction.

Puttable instrument: a financial instrument that gives the holder the right to put the instrument back to the issuer for cash or another financial asset or is automatically put back to the issuer on occurrence of an uncertain future event or the death or retirement of the instrument holder.

Classification as liability or equity

The fundamental principle of IAS 32 is that a financial instrument should be classified as either a financial liability or an equity instrument according to the substance of the contract, not its legal form, and the definitions of financial liability and equity instrument. Two exceptions from this principle are certain puttable instruments meeting specific criteria and certain obligations arising on liquidation. The entity must make the decision at the time the instrument is initially recognized. The classification is not subsequently changed based on changed circumstances.

A financial instrument is an equity instrument only if (a) the instrument includes no contractual obligation to deliver cash or another financial asset to another entity and (b) if the instrument will or may be settled in the issuer's own equity instruments, it is either:

37

a non-derivative that includes no contractual obligation for the issuer to deliver a variable number of its own equity instruments; or

a derivative that will be settled only by the issuer exchanging a fixed amount of cash or another financial asset for a fixed number of its own equity instruments.

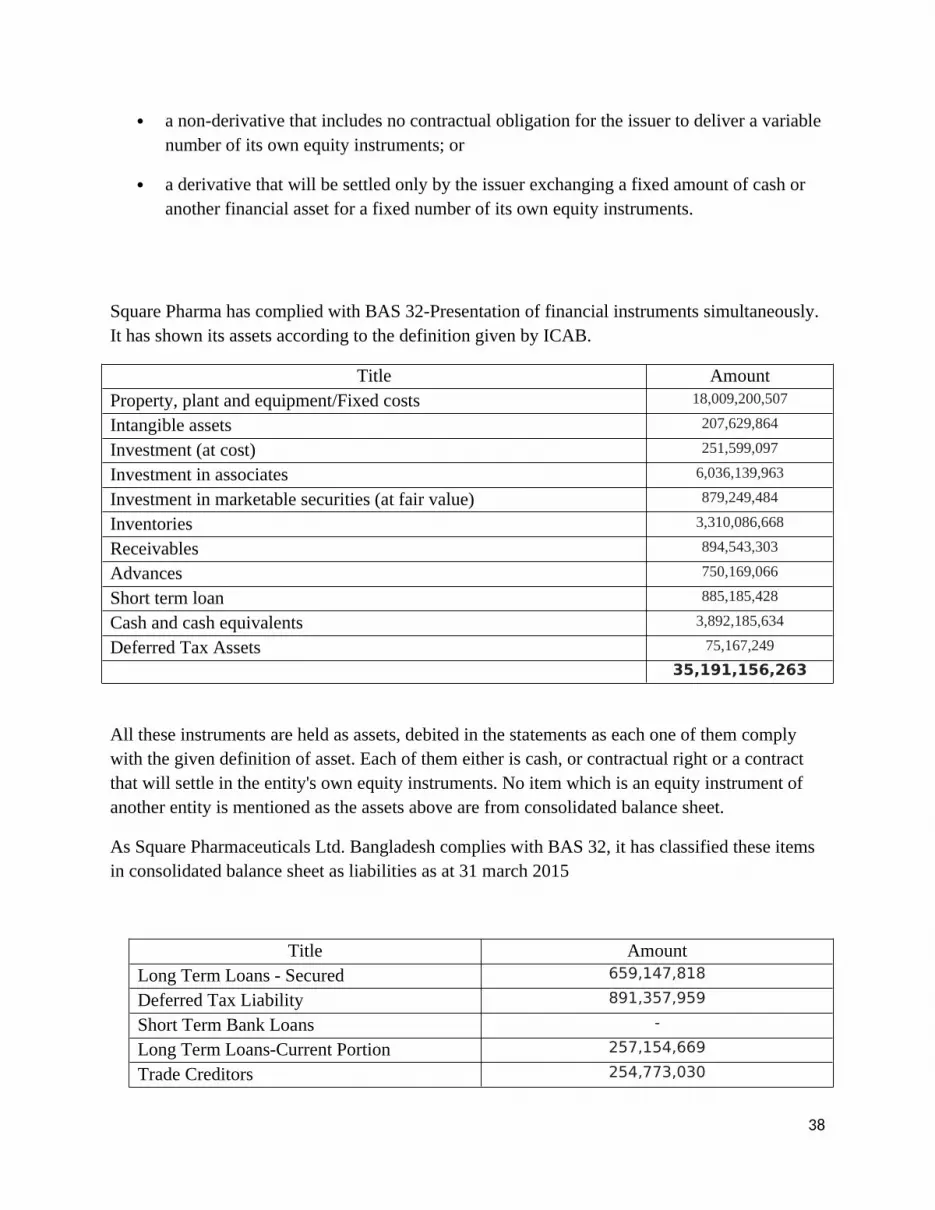

Square Pharma has complied with BAS 32-Presentation of financial instruments simultaneously. It has shown its assets according to the definition given by ICAB.

Title AmountProperty, plant and equipment/Fixed costs 18,009,200,507

Intangible assets 207,629,864

Investment (at cost) 251,599,097

Investment in associates 6,036,139,963

Investment in marketable securities (at fair value) 879,249,484

Inventories 3,310,086,668

Receivables 894,543,303

Advances 750,169,066

Short term loan 885,185,428

Cash and cash equivalents 3,892,185,634

Deferred Tax Assets 75,167,249

35,191,156,263

All these instruments are held as assets, debited in the statements as each one of them comply with the given definition of asset. Each of them either is cash, or contractual right or a contract that will settle in the entity's own equity instruments. No item which is an equity instrument of another entity is mentioned as the assets above are from consolidated balance sheet.

As Square Pharmaceuticals Ltd. Bangladesh complies with BAS 32, it has classified these items in consolidated balance sheet as liabilities as at 31 march 2015

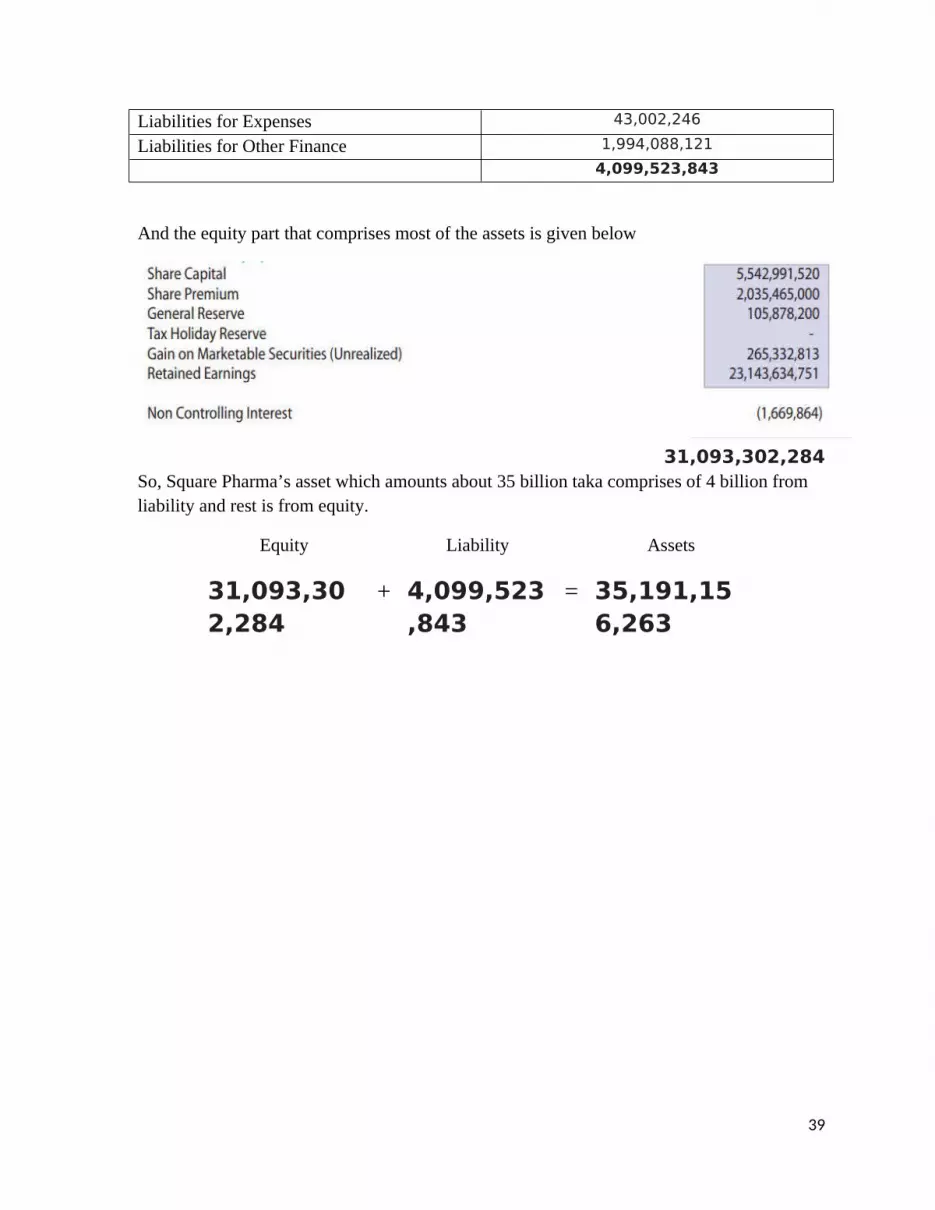

Title AmountLong Term Loans - Secured 659,147,818Deferred Tax Liability 891,357,959Short Term Bank Loans -Long Term Loans-Current Portion 257,154,669Trade Creditors 254,773,030

38

Liabilities for Expenses 43,002,246Liabilities for Other Finance 1,994,088,121

4,099,523,843

And the equity part that comprises most of the assets is given below

31,093,302,284So, Square Pharma’s asset which amounts about 35 billion taka comprises of 4 billion from liability and rest is from equity.

Equity Liability Assets

31,093,302,284

+ 4,099,523,843

= 35,191,156,263

39

BAS 33

Earnings Per Share

Theoretical Overview:

Earnings per share (EPS) is the portion of a company's profit allocated to each outstanding share of common stock. Earnings per share serve as an indicator of a company's profitability.

Objective:

The objective of BAS 33 is to prescribe principles for determining and presenting earnings per share (EPS) amounts to improve performance comparisons between different entities in the same reporting period and between different reporting periods for the same entity. [BAS 33.1]

Scope

BAS 33 applies to entities whose securities are publicly traded or that are in the process of issuing securities to the public. [BAS 33.2] Other entities that choose to present EPS information must also comply with BAS 33. [BAS 33.3]

If both parent and consolidated statements are presented in a single report, EPS is required only for the consolidated statements. [BAS 33.4]

Dilution: a reduction in earnings per share or an increase in loss per share resulting from the assumption that convertible instruments are converted, that options or warrants are exercised, or that ordinary shares are issued upon the satisfaction of specified conditions.

Anti-dilution: An increase in earnings per share or a reduction in loss per share resulting from the assumption that convertible instruments are converted, thatoptions or warrants are exercised, or that ordinary sharesare issued upon the satisfaction of specified conditions.

Requirement to present EPS

An entity whose securities are publicly traded (or that is in process of public issuance) must present, on the face of the statement of comprehensive income, basic and diluted EPS for: [BAS 33.66]

If an entity presents the components of profit or loss in a separate income statement, it presents EPS only in that separate statement. [BAS 33.4A]

40

Basic and diluted EPS must be presented with equal prominence for all periods presented. [BAS 33.66]

Basic and diluted EPS must be presented even if the amounts are negative (that is, a loss per share). [BAS33.69]

If an entity reports a discontinued operation, basic and diluted amounts per share must be disclosed for the discontinued operation either on the face of the comprehensive income (or separate income statement if presented) or in the notes to the financial statements. [BAS 33.68 and 68A]

Basic EPS

Basic EPS is calculated by dividing profit or loss attributable to ordinary equity holders of the parent entity (the numerator) by the weighted average number of ordinary shares outstanding (the denominator) during the period. [BAS 33.10]

Diluted EPS

Diluted EPS is calculated by adjusting the earnings and number of shares for the effects of dilutive options and other dilutive potential ordinary shares. [BAS 33.31] The effects of anti-dilutive potential ordinary shares are ignored in calculating diluted EPS. [BAS 33.41]

Square pharmaceuticals Limited’s Compliance with BAS 33

The company calculates their EPS based on the standard BAS 33. It has calculated the EPS using formula

Profit after tax

Weighted average number of Shares outstanding during the year

41

EARNINGS PER SHARE (EPS): 2014-2015 2013-2014

Surplus for the year attributable to Shareholders (Net Profit after Tax)

5,743,623,832 4,031,811,268

Weighted average number of Shares outstanding during the year

554,299,152 554,299,152

Earnings per Share 10.36 7.27

Calculating the Profit and Number of shares putting on the formula we have found the Earning per share for the year 2014-2015 is 10.36 and for 2013-2014 is 7.27. They have complied with the BAS 33 properly.

Again company has used current year’s weighted average number of shares outstanding as a base for both years to have a good comparison of EPS between the two consecutive years. They had 4,819,992,630 shares for 2013 to 2014. But they have taken 554299152 shares for both years so that they can compare the company’s performance for the both years.\

Diluted Earnings per Share

No diluted Earnings per Share was required to be calculated for the year under review as there is no scope for dilution of Earnings Per Share for the year.

42

BAS 37

Provisions, Contingent Liabilities and ContingentAsset

BAS 37 aims to ensure that: Appropriate recognition criteria and measurement bases are applied to provisions,

contingent assets and contingent liabilities; and Sufficient information is disclosed in the notes to the financial statements to enable users

to understand their nature, timing and amount.

Provisions:A provision is a liability of uncertain timing oramount. A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits

Recognition of Provision: BAS 37 states that a provision should be recognized when: An entity has a present obligation (legal or constructive) as a result of a past event It is probable that an outflow of resources embodying economic benefits will be required

to settle the obligation; and A reliable estimate can be made of the amount of the obligation

Contingent Liability:A contingent liability is either:

A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity, or A present obligation that arises from past events but is not recognized becausea) It is not probable that an outflow of resources embodying economic benefits will

be required to settle the obligation; orb) The amount of the obligation cannot be measured with sufficient reliability.

Contingent Assets:A contingent asset is a possible asset that arises from pastevents and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

Square Pharmaceuticals Limited’s Compliance with BAS 37Square Pharmaceuticals Limited has been complied with the BAS 37 to recognize and measure provision and contingent liabilities.

Provisions, Contingent Liabilities and Contingent Assets:

43

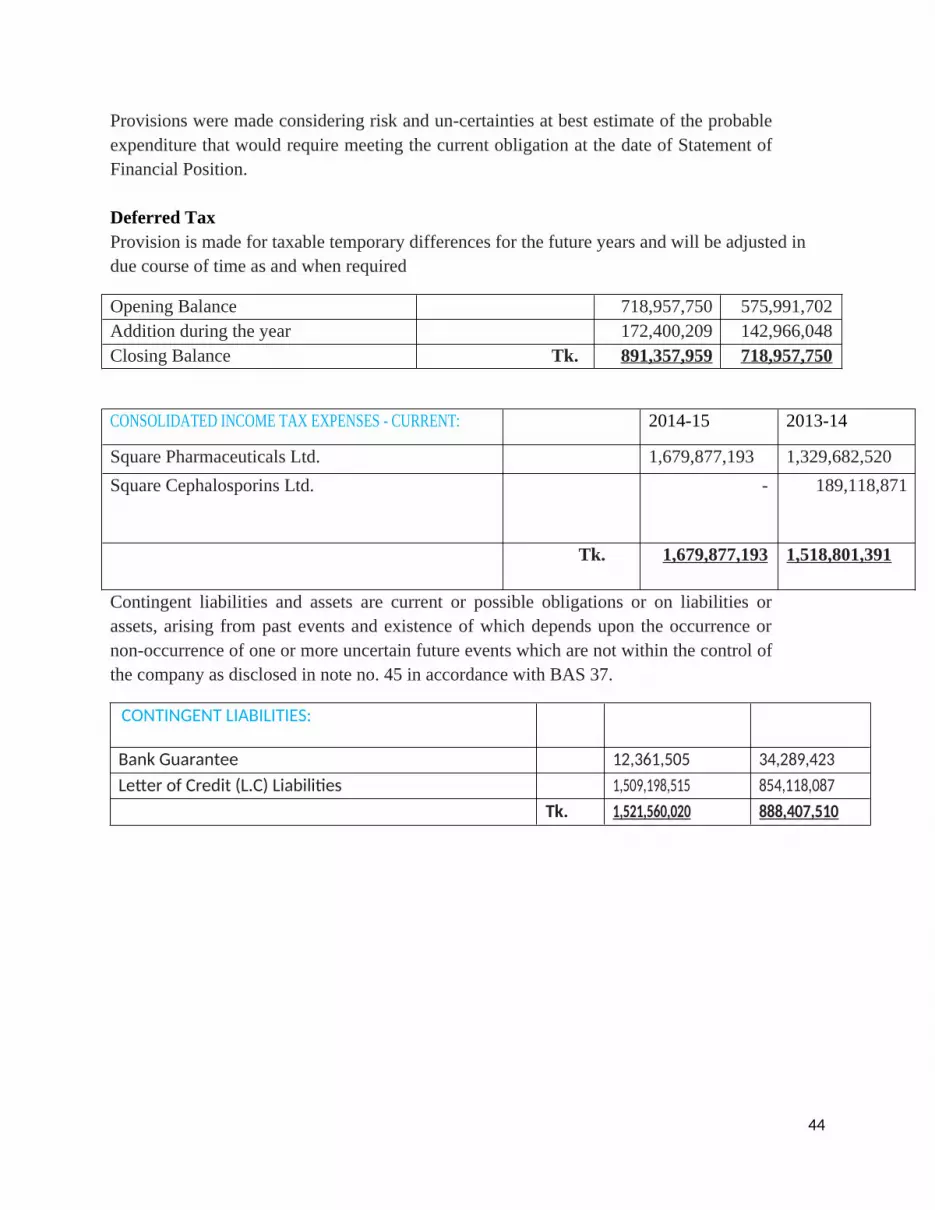

Provisions were made considering risk and un-certainties at best estimate of the probable expenditure that would require meeting the current obligation at the date of Statement of Financial Position.

Deferred TaxProvision is made for taxable temporary differences for the future years and will be adjusted in due course of time as and when required

Opening Balance 718,957,750 575,991,702Addition during the year 172,400,209 142,966,048Closing Balance Tk. 891,357,959 718,957,750

CONSOLIDATED INCOME TAX EXPENSES - CURRENT: 2014-15 2013-14

Square Pharmaceuticals Ltd. 1,679,877,193 1,329,682,520Square Cephalosporins Ltd. - 189,118,871

Tk. 1,679,877,193 1,518,801,391

Contingent liabilities and assets are current or possible obligations or on liabilities or assets, arising from past events and existence of which depends upon the occurrence or non-occurrence of one or more uncertain future events which are not within the control of the company as disclosed in note no. 45 in accordance with BAS 37.

CONTINGENT LIABILITIES:

Bank Guarantee 12,361,505 34,289,423Letter of Credit (L.C) Liabilities 1,509,198,515 854,118,087

Tk. 1,521,560,020 888,407,510

44

BAS 38

Intangible Assets

An Intangible Asset is an identifiable non-monetary asset without physical substance.

Intangible assets include items such as:

Licenses & quotas Intellectual property, e.g. patents & copyrights Brand names Trademarks

For an asset to be identifiable, it must fall into one of two categories:

It is separable- the asset can be bought or sold separately from the rest of the business It arises from legal/contractual rights.

It must also meet the normal definition of an asset:

Controlled by the entity as a result of past events A resource from which future economic benefits are expected to flow.

Recognition:

To be recognized in the financial statements, an intangible asset must:

Meet the definition of intangible asset, and Meet the recognition criteria of the framework

If these criteria are met, the asset should be initially recognized at cost.

Purchased Intangibles:

If an intangible is purchased separately (such as license, patent, brand name), itshould be recognized initially at cost.

Measurement after initial recognition:

There is a choice between:

The cost model The revaluation model

The cost model:

45

Under this model, the intangible asset should be carried at cost less amortization and any impairment losses. This model is more commonly used in practice.

An intangible asset with a finite useful life must be amortized over that life, normally using the straight- line method with a zero residual value.

An intangible asset with an indefinite useful life:

Should not be amortized Should be tested for impairment annually and more often if there is an actual indication

of possible impairment.

The revaluation model:

The intangible asset may be revalued to a carrying amount of fair value less subsequent amortization and impairment losses. The fair value should be determined by reference to an active market.

Internally- generated intangibles:

Generally, internally generated intangibles cannot be capitalized, as costs associated with these cannot be separated from the costs associated with running the business.

The following internally-generated items may never be recognized:

Goodwill Brands Mastheads Publishing titles Customer lists.

Research & Development:

Research is original & planned investigation undertaken with the prospect of gaining new scientific knowledge and understanding.

Development is the applicationof research findings or other knowledge to a plan or design for the production of new or substantially improved materials, devices, products, processes, systems or services before the start of commercial production or use.

Accounting treatment:

Research expenditure: written off as incurred to the statement of profit & loss.

46

Development expenditure:recognized as an intangible asset if, and only if, an entity can demonstrate all of the following:

Probable future economic benefits from the asset, whether through sale or internal cost saving.

Intention to complete the intangible asset and use or sell it. Resource available to complete the development and to use or sell the intangible asset. Ability to use or sell the intangible etc.

Amortization:

Development expenditure should be amortized over its useful life as soon as commercial production begins.

Square Pharmaceuticals Limited’s compliance with BAS 38:

In compliance with the requirement of BAS38, Square Pharmaceuticals Ltd absorbs ‘Intangible Assets’ research, development & experimental costs as revenue charges as and when incurred, which is not much material in the company’s and/local context.

47

BFRS 7

Financial Instruments:Disclosure

Notes are fundamental to the financial statements. The purpose of financial statements is to provide economic data to various concerned party about its financial position, changes in financial position and earnings in the year. To do that properly, notes are to be provided. As without notes, it would be impossible to draw conclusions or make decisions properly. Because financial statements only represent numeric facts. Notes are there to provide backup story. So, it is essential that an entity maintains and delivers its notes regularly. This essentiality refers to BFRS 7-Financial instruments: Disclosure. This standard states how exactly the notes would be published and maintained.

IFRS 7:

adds certain new disclosures about financial instruments to those previously required by IAS 32 Financial Instruments: Disclosure and Presentation

replaces the disclosures previously required by IAS 30 Disclosures in the Financial Statements of Banks and Similar Financial Institutions

Puts all of those financial instruments disclosures together in a new standard on Financial Instruments: Disclosures. The remaining parts of IAS 32 deal only with financial instruments presentation matters.

Disclosure requirements of IFRS 7

IFRS requires certain disclosures to be presented by category of instrument based on the IAS 39 measurement categories. Certain other disclosures are required by class of financial instrument. For those disclosures an entity must group its financial instruments into classes of similar instruments as appropriate to the nature of the information presented.

The two main categories of disclosures required by IFRS 7 are:

1. Information about the significance of financial instruments.

2. information about the nature and extent of risks arising from financial instruments

3. Information about the significance of financial instruments

Statement of financial position

Disclose the significance of financial instruments for an entity's financial position and performance. This includes disclosures for each of the following categories:

48

o financial assets measured at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition

o held-to-maturity investments

o loans and receivables

o available-for-sale assets

o financial liabilities at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition

o financial liabilities measured at amortized cost

Statement of comprehensive income

Items of income, expense, gains, and losses, with separate disclosure of gains and losses from:

o Financial assets measured at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition.

o Held-to-maturity investments.

o Loans and receivables.

o Available-for-sale assets.

o Financial liabilities measured at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition.

o Financial liabilities measured at amortised cost.

Here are some disclosures related to consolidated balance sheet of Square Pharma Ltd.

Determining carrying value of fixed assets

49

CONSOLIDATED CAPITAL WORK-IN-PROGRESS:

Associated Undertakings:

50

51

Investment

s

Cost of goods sold

52

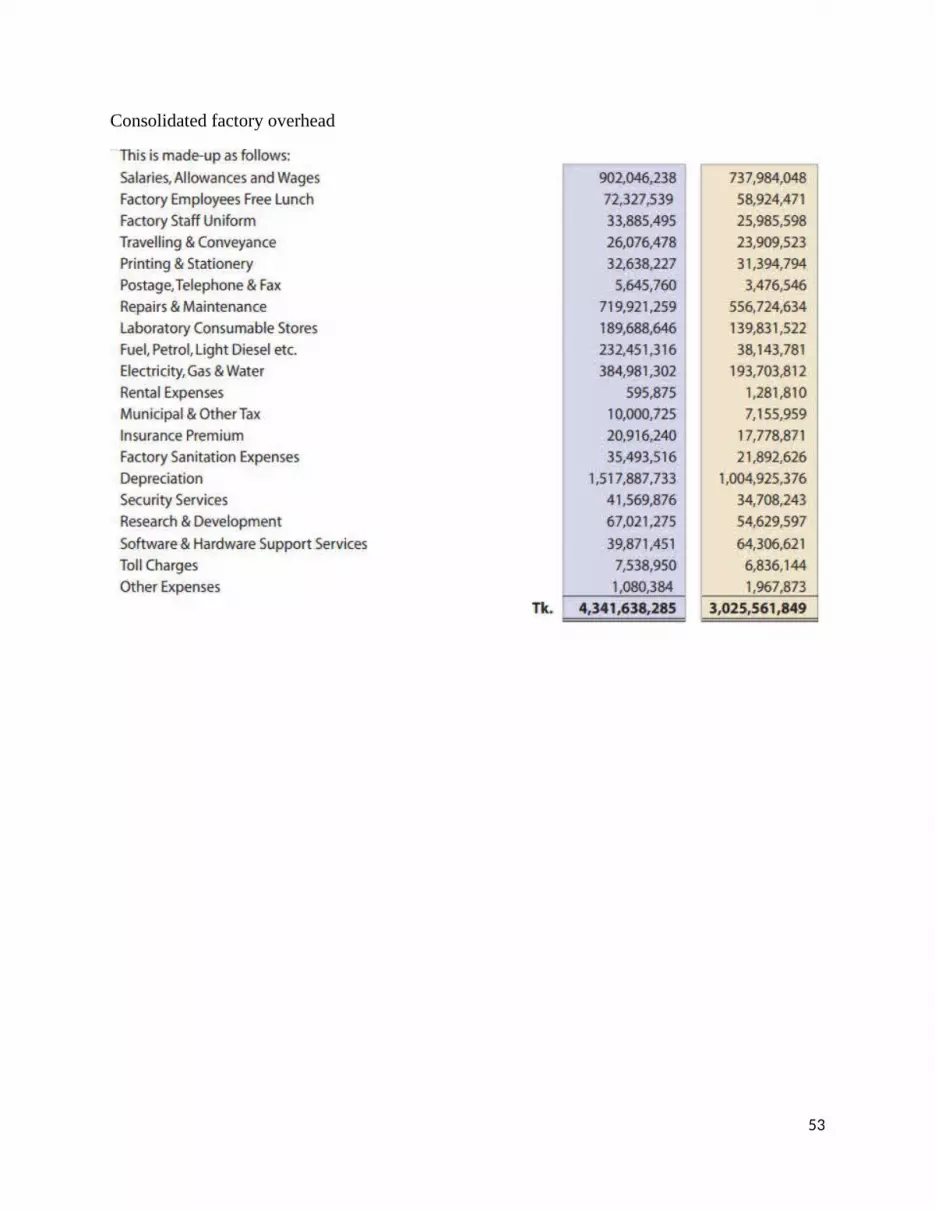

Consolidated factory overhead

53

BFRS 10

Consolidated Financial Statements

Theoretical overview

IFRS 10 Consolidated Financial Statements outlines the requirements for the preparation and presentation of consolidated financial statements, requiring entities to consolidate entities it controls. Control requires exposure or rights to variable returns and the ability to affect those returns through power over an investee.

Objective

The objective of IFRS 10 is to establish principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities

The Standard:

It requires a parent entity (an entity that controls one or more other entities) to present consolidated financial statements defines the principle of control, and establishes control as the basis for consolidation set out how to apply the principle of control to identify whether an investor controls an investee and therefore must consolidate the investee sets out the accounting requirements for the preparation of consolidated financial statements defines an investment entity and sets out an exception to consolidating particular subsidiaries of an investment entity

Consolidated financial statements:

The financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity.

Control of an investee:

An investor controls an investee when the investor is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee

Investment Entity:

An entity that:

a. Obtains funds from one or more investors for the purpose of providing those investor(s) with investment management services

b. Commits to its investor(s) that its business purpose is to invest funds solely for returns from capital appreciation, investment income, or both, and

54

c. Measures and evaluates the performance of substantially all of its investments on a fair value basis.

Parent

An entity that controls one or more entities

Power

Existing rights that give the current ability to direct the relevant activities

Protective rights

Rights designed to protect the interest of the party holding those rights without giving that party power over the entity to which those rights relate.

Relevant activities

Activities of the investee that significantly affect the investee's returns

Control

An investor determines whether it is a parent by assessing whether it controls one or more investees. An investor considers all relevant facts and circumstances when assessing whether it controls an investee. An investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee.

An investor controls an investee if and only if the investor has all of the following elements:

Power over the investee: the investor has existing rights that give it the ability to direct the relevant activities (the activities that significantly affect the investee's returns)

Exposure, or rights, to variable returns from its involvement with the investee The ability to use its power over the investee to affect the amount of the investor's

returns.

Power arises from rights. Such rights can be straightforward (e.g. through voting rights) or be complex (e.g. embedded in contractual arrangements). An investor that holds only protective rights cannot have power over an investee and so cannot control an investee.

An investor must be exposed, or have rights, to variable returns from its involvement with an investee to control the investee. Such returns must have the potential to vary as a result of the investee's performance and can be positive, negative, or both

55

A parent must not only have power over an investee and exposure or rights to variable returns from its involvement with the investee, a parent must also have the ability to use its power over the investee to affect its returns from its involvement with the investee

When assessing whether an investor controls an investee an investor with decision-making rights determines whether it acts as principal or as an agent of other parties. A number of factors are considered in making this assessment. For instance, the remuneration of the decision-maker is considered in determining whether it is an agent.

Accounting requirements

Preparation of consolidated financial statements

A parent prepares consolidated financial statements using uniform accounting policies for like transactions and other events in similar circumstances.

Consolidation procedures

Consolidated financial statements:

Consolidated financial statements combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent with those of its subsidiaries offset (eliminate) the carrying amount of the parent's investment in each subsidiary and the parent's portion of equity of each subsidiary (IFRS 3 Business Combinations explains how to account for any related goodwill) eliminate in full intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group (profits or losses resulting from intra group transactions that are recognized in assets, such as inventory and fixed assets, are eliminated in full).

A reporting entity includes the income and expenses of a subsidiary in the consolidated financial statements from the date it gains control until the date when the reporting entity ceases to control the subsidiary. Income and expenses of the subsidiary are based on the amounts of the assets and liabilities recognized in the consolidated financial statements at the acquisition date.

The parent and subsidiaries are required to have the same reporting dates, or consolidation based on additional financial information prepared by subsidiary, unless impracticable. Where impracticable, the most recent financial statements of the subsidiary are used, adjusted for the effects of significant transactions or events between the reporting dates of the subsidiary and consolidated financial statements. The difference between the date of the subsidiary's financial statements and that of the consolidated financial statements shall be no more than three months.

56

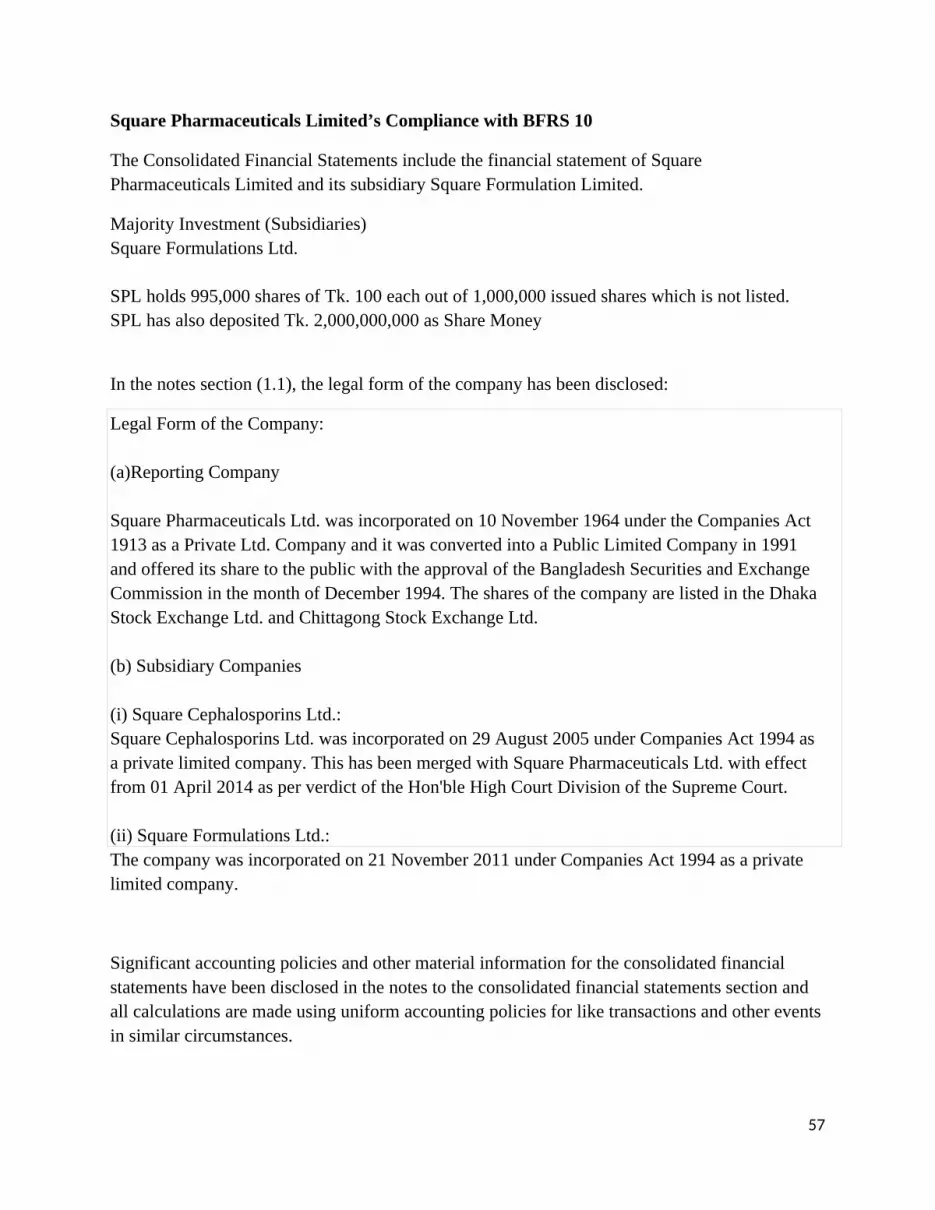

Square Pharmaceuticals Limited’s Compliance with BFRS 10

The Consolidated Financial Statements include the financial statement of Square Pharmaceuticals Limited and its subsidiary Square Formulation Limited.

Majority Investment (Subsidiaries)Square Formulations Ltd.

SPL holds 995,000 shares of Tk. 100 each out of 1,000,000 issued shares which is not listed. SPL has also deposited Tk. 2,000,000,000 as Share Money

In the notes section (1.1), the legal form of the company has been disclosed:

Legal Form of the Company:

(a)Reporting Company

Square Pharmaceuticals Ltd. was incorporated on 10 November 1964 under the Companies Act 1913 as a Private Ltd. Company and it was converted into a Public Limited Company in 1991 and offered its share to the public with the approval of the Bangladesh Securities and Exchange Commission in the month of December 1994. The shares of the company are listed in the Dhaka Stock Exchange Ltd. and Chittagong Stock Exchange Ltd.

(b) Subsidiary Companies

(i) Square Cephalosporins Ltd.:Square Cephalosporins Ltd. was incorporated on 29 August 2005 under Companies Act 1994 as a private limited company. This has been merged with Square Pharmaceuticals Ltd. with effect from 01 April 2014 as per verdict of the Hon'ble High Court Division of the Supreme Court.

(ii) Square Formulations Ltd.:The company was incorporated on 21 November 2011 under Companies Act 1994 as a private limited company.

Significant accounting policies and other material information for the consolidated financial statements have been disclosed in the notes to the consolidated financial statements section and all calculations are made using uniform accounting policies for like transactions and other events in similar circumstances.

57

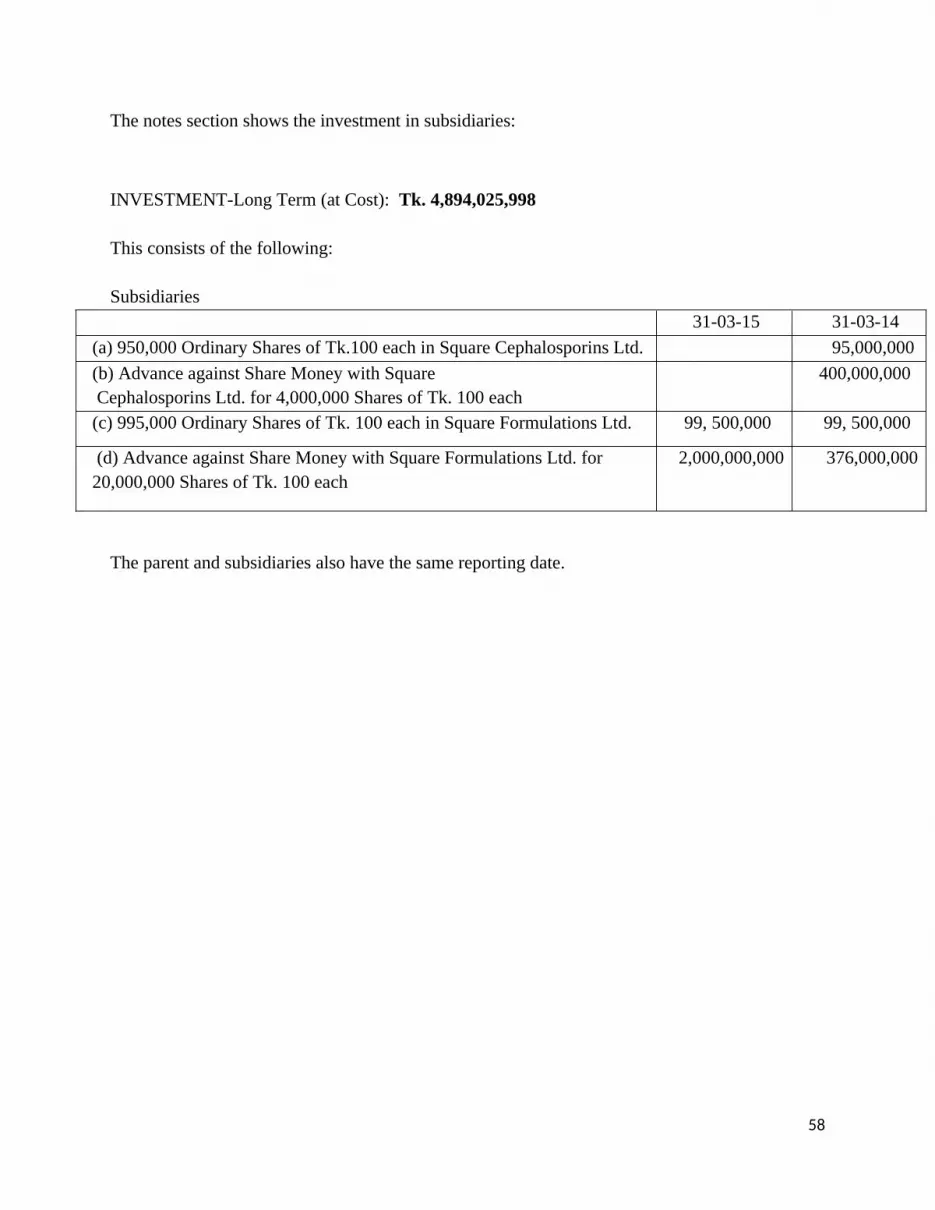

The notes section shows the investment in subsidiaries:

INVESTMENT-Long Term (at Cost): Tk. 4,894,025,998

This consists of the following:

Subsidiaries 31-03-15 31-03-14

(a) 950,000 Ordinary Shares of Tk.100 each in Square Cephalosporins Ltd. 95,000,000(b) Advance against Share Money with Square Cephalosporins Ltd. for 4,000,000 Shares of Tk. 100 each

400,000,000

(c) 995,000 Ordinary Shares of Tk. 100 each in Square Formulations Ltd. 99, 500,000 99, 500,000

(d) Advance against Share Money with Square Formulations Ltd. for20,000,000 Shares of Tk. 100 each

2,000,000,000 376,000,000

The parent and subsidiaries also have the same reporting date.

58

Chapter 4

Compliance with BAS and BFRS

59

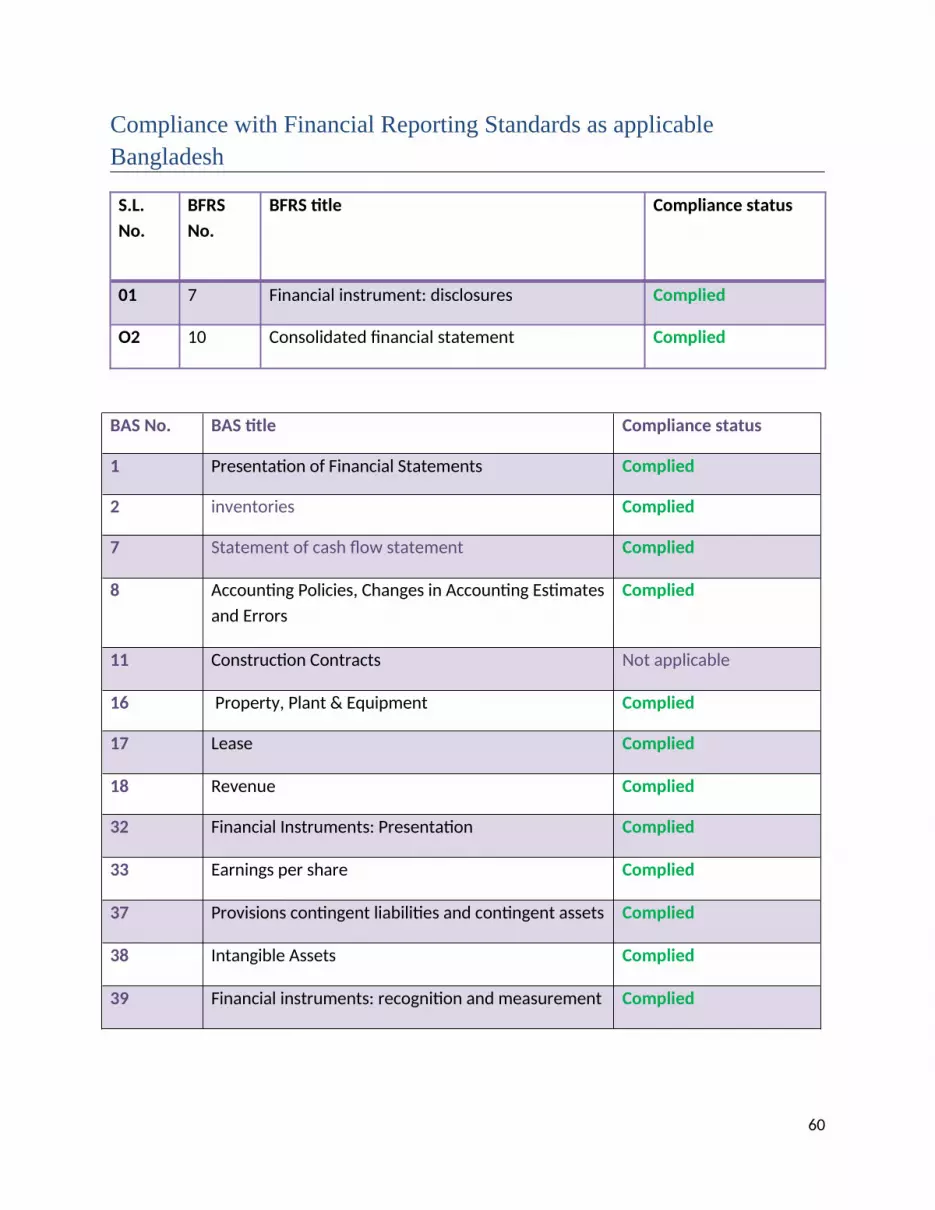

Compliance with Financial Reporting Standards as applicable Bangladesh

S.L. No.

BFRS No.

BFRS title Compliance status

01 7 Financial instrument: disclosures Complied

O2 10 Consolidated financial statement Complied

BAS No. BAS title Compliance status

1 Presentation of Financial Statements Complied

2 inventories Complied

7 Statement of cash flow statement Complied

8 Accounting Policies, Changes in Accounting Estimates and Errors

Complied

11 Construction Contracts Not applicable

16 Property, Plant & Equipment Complied

17 Lease Complied

18 Revenue Complied

32 Financial Instruments: Presentation Complied

33 Earnings per share Complied

37 Provisions contingent liabilities and contingent assets Complied

38 Intangible Assets Complied

39 Financial instruments: recognition and measurement Complied

60

Chapter 5

Conclusion

Throughout the term paper we have tried our best to prove our skill acquired from F201, Financial Accounting and Reporting course. We have put our sincere effort to give this report a presentable shape and make it as precise as possible. We cordially thank our honorable faculty for providing us with this unique opportunity.

61